Why Wealthy Investors Borrow Against Their Portfolio - and When It Backfires

We get asked about these regularly. A client hears about them from a friend, someone mentions it in a meeting, or someone reads that wealthy investors use them to avoid selling appreciated positions. The concept sounds elegant. Borrow against what you already own, stay invested, skip the tax event.

And in the right situation, with the right structure, they can be exactly that. But we’ve also seen them go wrong in ways that are genuinely painful - forced sales near market bottoms, unexpected tax bills, and portfolios that looked comfortable until the market moved and suddenly weren’t.

This week we’re breaking down how securities-backed lines of credit actually work, what the risk mechanics look like in practice, and the patterns we see most often when they become a problem.

Let’s dig in

What an SBLOC Actually Is

A securities-backed line of credit lets you borrow against your taxable brokerage account - typically up to 50-70% of its value, depending on what you hold. The credit line opens. Your portfolio stays invested. No securities are sold. No taxable event is triggered at origination.

For high earners with concentrated, appreciated positions, the appeal is straightforward. You need liquidity - for a real estate deal, a business opportunity, a bridge between transactions - but selling to raise cash means triggering capital gains on positions you’ve held for years. An SBLOC offers a third option: access the capital without selling.

On paper, the math can work. In practice, the outcome depends almost entirely on what happens after you borrow.

How the Collateral Mechanics Work

Lenders assign a lendable value to each security in your portfolio - typically 50-70% of market value for equities, though concentrated positions, less liquid holdings, or more volatile securities may receive lower lendable values.

On a $2 million portfolio at 65% lendable value, your maximum line may be approximately $1.3 million. That’s illustrative - actual terms vary by lender, account composition, and your overall relationship.

Here’s where it gets important: that lendable value moves with the market. It isn’t fixed at origination. When your portfolio value drops, your lendable value drops with it. And if it drops far enough that the lendable value falls below your outstanding loan balance, a maintenance call may come.

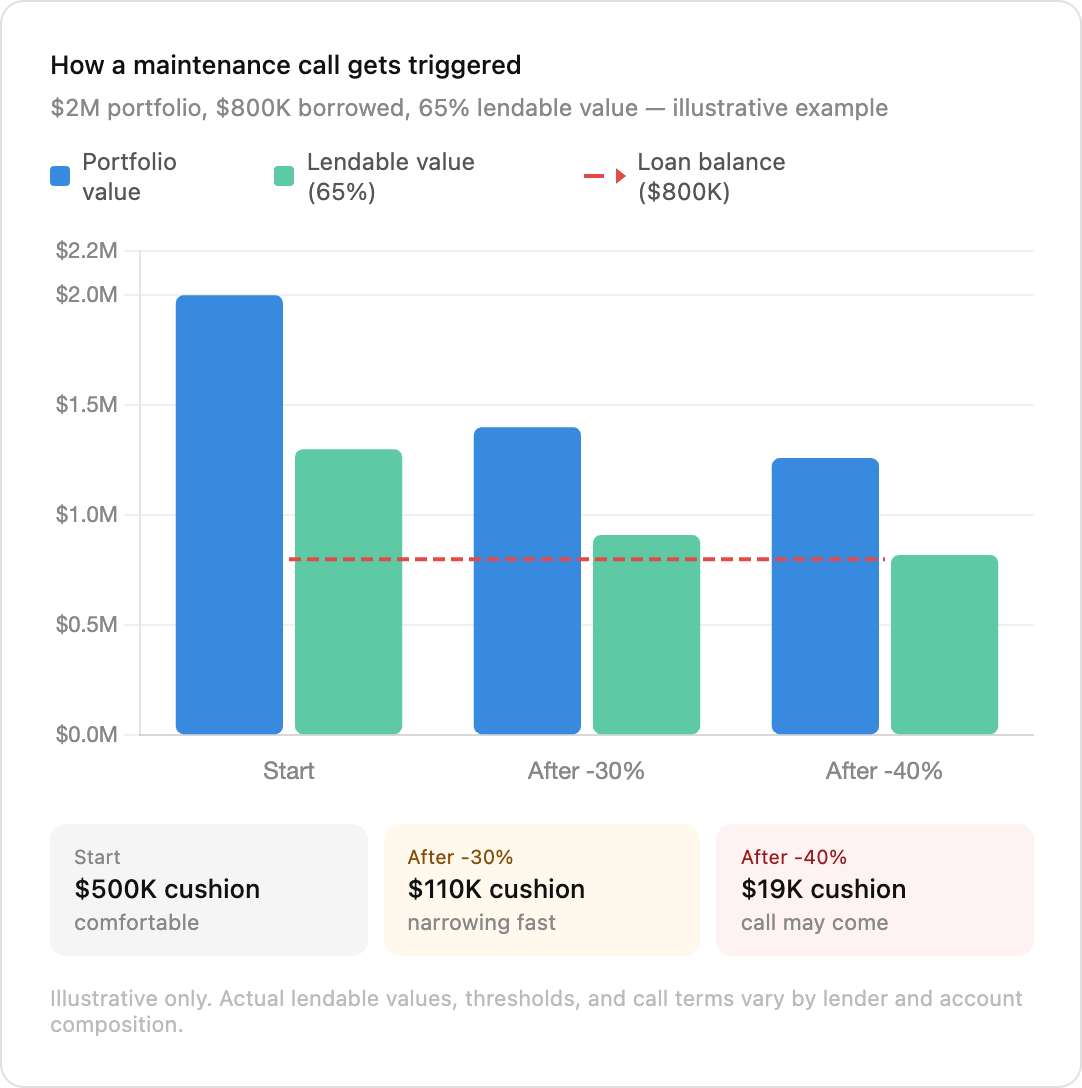

What a Maintenance Call Actually Looks Like

This is the scenario most people don’t fully think through when they open the line.

Say you borrow $800,000 against a $2 million portfolio. At 65% lendable value, your collateral supports approximately $1.3 million. You have meaningful cushion.

Markets drop 30%. Your portfolio is now worth $1.4 million. Lendable value: approximately $910,000. Still above your $800,000 balance - but the buffer has narrowed considerably.

Another 10% decline. Portfolio: approximately $1.26 million. Lendable value: approximately $819,000. You’re approaching the threshold.

One more move down, and the call may come. When it does, you typically have two to three days to respond. Your options at that point are generally to deposit cash to restore the collateral cushion, deposit additional securities, or repay part of the loan.

If you can’t do any of those - the lender may sell your securities. They may choose which positions to sell. At whatever price the market is offering at that moment.

Why Forced Liquidation Can Make a Bad Situation Worse

Here’s what makes a maintenance call scenario particularly damaging. The market has just dropped - that’s what triggered the call. And now positions you’ve held for years, with embedded long-term gains, may be sold near that bottom.

The result may include a portfolio that’s down 30-40%, forced sales at depressed prices, and a capital gains tax bill arriving in the same calendar year. The portfolio took the loss and generated the tax liability simultaneously.

This isn’t a hypothetical worst case. It’s a sequence of events that played out for a number of SBLOC borrowers in 2022.

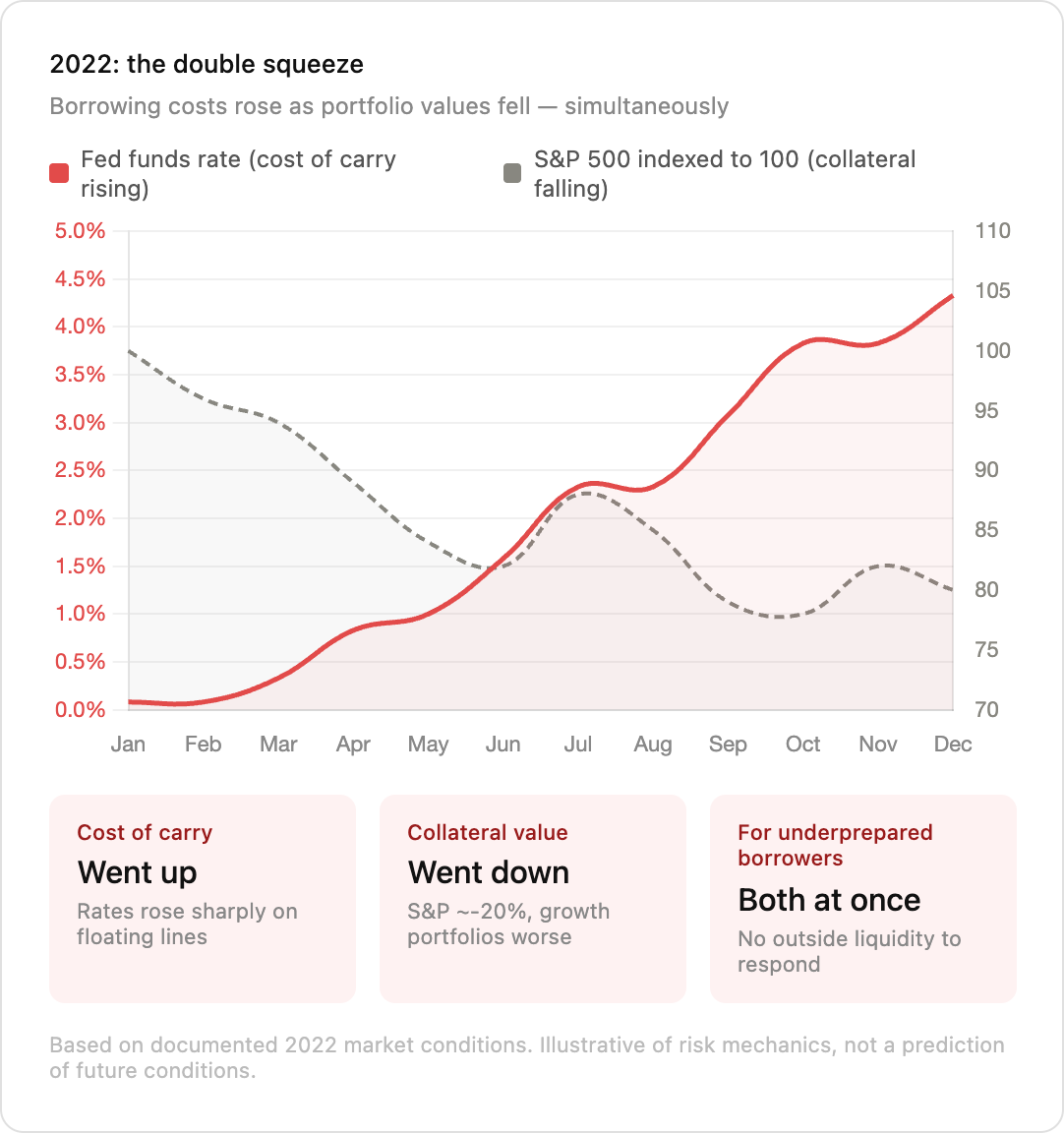

2022: The Double Squeeze

2022 illustrated a specific risk that floating-rate SBLOC borrowers didn’t fully account for going in.

The Federal Reserve raised rates sharply throughout the year. Borrowing costs on floating rate lines increased significantly - in some cases doubling or more from where they started.

At the same time, the S&P 500 dropped approximately 20% on the year. Growth-heavy portfolios fared considerably worse. For borrowers with concentrated technology or growth positions pledged as collateral, the lendable value decline was more severe than the headline index suggested.

Both happened simultaneously. The cost of carrying the loan went up. The collateral supporting it went down. For borrowers who had structured the line with little buffer and no outside liquidity, that combination created real pressure very quickly.

When SBLOCs May Make Sense

This isn’t a tool to avoid categorically. For the right borrower in the right situation, an SBLOC may be a genuinely useful liquidity tool.

Situations where they may make sense include short-term bridge financing where liquidity is arriving in a defined timeframe - a property closing, a business sale, a bonus - and the line is being used to bridge a known gap. They may also make sense when the alternative is triggering a large capital gains event on a long-held position, and the borrower has significant liquid assets outside the pledged portfolio to meet a potential call without touching it.

The key question is this: if markets dropped 30-40% tomorrow, could you repay or post additional collateral without selling from the pledged portfolio? If the honest answer is no, that’s worth sitting with before drawing on the line.

Patterns We See Go Wrong

In working with clients who’ve used or considered SBLOCs, a few patterns come up when things go sideways.

Borrowing the maximum with no buffer for a market decline. The lendable value at origination is a ceiling, not a target - most advisors would suggest borrowing well below it to preserve room for portfolio movement.

Using the line for ongoing expenses with no repayment plan. An SBLOC structured as a revolving credit facility for lifestyle spending, with no mechanism to pay it down, is leverage that compounds over time.

Pledging the entire taxable portfolio with nothing outside. If the only assets available to meet a maintenance call are inside the pledged account, every market decline becomes a potential forced liquidation scenario.

Assuming the line stays open. Lenders may reduce or freeze the line at any time - often precisely when markets are declining and you might most want to access it.

Missing the floating rate risk. If rates rise while you’re carrying a balance, the cost of the loan increases whether you want it to or not.

Bottom Line

SBLOCs are marketed as a sophisticated wealth management tool. For a specific type of borrower - one with significant liquidity outside the pledged portfolio, a defined repayment timeline, and a clear purpose for the capital - they may live up to that description.

But leverage on a volatile asset, no repayment plan, and no outside liquidity is a combination that can unravel quickly when markets move. And markets always move eventually.

SBLOCs let you borrow against a taxable portfolio - typically 50-70% of lendable value - without selling or triggering a taxable event at origination

Lendable value moves with the market - a significant decline may trigger a maintenance call requiring cash, additional collateral, or loan repayment within days

If you can’t meet a call, the lender may sell your positions at depressed prices, potentially triggering taxable gains in the same year

2022 demonstrated a double squeeze - rising rates increased carry costs while falling markets reduced collateral simultaneously

The borrowers most at risk are those without liquidity outside the pledged account and no defined repayment plan

Before considering an SBLOC, the most important question to ask isn’t “how much can I borrow?” It’s “what happens to this plan if markets drop 30% next month?”

If the answer is uncomfortable, that discomfort is useful information.

See you next week.

- Fran

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 3,200+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.

Awesome post and really helpful!

Great read, Franny!