Two Siblings. Same Inheritance. A $277,000 Difference in Taxes.

The SECURE Act changed the rules on inherited IRAs. Most beneficiaries still don't know it.

A few months ago, I sat across from someone who had just inherited a $500,000 IRA from her father. She was relieved - grateful, even. It felt like a gift, a cushion, a head start she didn’t expect.

By the time we mapped out what her tax bill could look like if she handled it the way most people do, the room got very quiet.

She wasn’t doing anything wrong. She was doing exactly what most people do - planning to let it grow for as long as possible and take it out when she needed it. The problem is that the rules changed in 2020, and nobody told her. The same goes for most of the people who inherit retirement accounts every year.

This week, we’re breaking down one of the most misunderstood tax situations we see - the inherited IRA - and what a thoughtful distribution strategy can mean for how much of that inheritance you actually keep.

Let’s dig in

What the SECURE Act Changed

Before 2020, inherited IRAs were genuinely powerful. Most non-spouse beneficiaries could “stretch” distributions across their lifetime - decades of continued tax-deferred growth, small annual withdrawals, minimal tax impact. It was one of the most effective wealth transfer tools available.

The SECURE Act largely ended that. For most non-spouse beneficiaries today, the account must be fully emptied within 10 years of the original owner’s death. That single change transformed an inherited IRA from a multigenerational planning tool into a 10-year tax management problem.

The clock is ticking whether you know about it or not.

Who the 10-Year Rule Does - and Doesn’t - Apply To

Before going further, it’s worth noting the exceptions, because they matter. The 10-year rule generally does not apply to surviving spouses, who have more flexible options including treating the IRA as their own. It also generally doesn’t apply to minor children of the account owner - though once they reach age 21, the 10-year clock typically begins. Beneficiaries who are disabled or chronically ill, and those within 10 years of age of the deceased, may also qualify for different treatment.

If you fall into one of those categories, your planning options look meaningfully different. For everyone else, the 10-year rule applies - and what you do within that window has significant consequences.

The Tax Bomb Most People Don’t See Coming

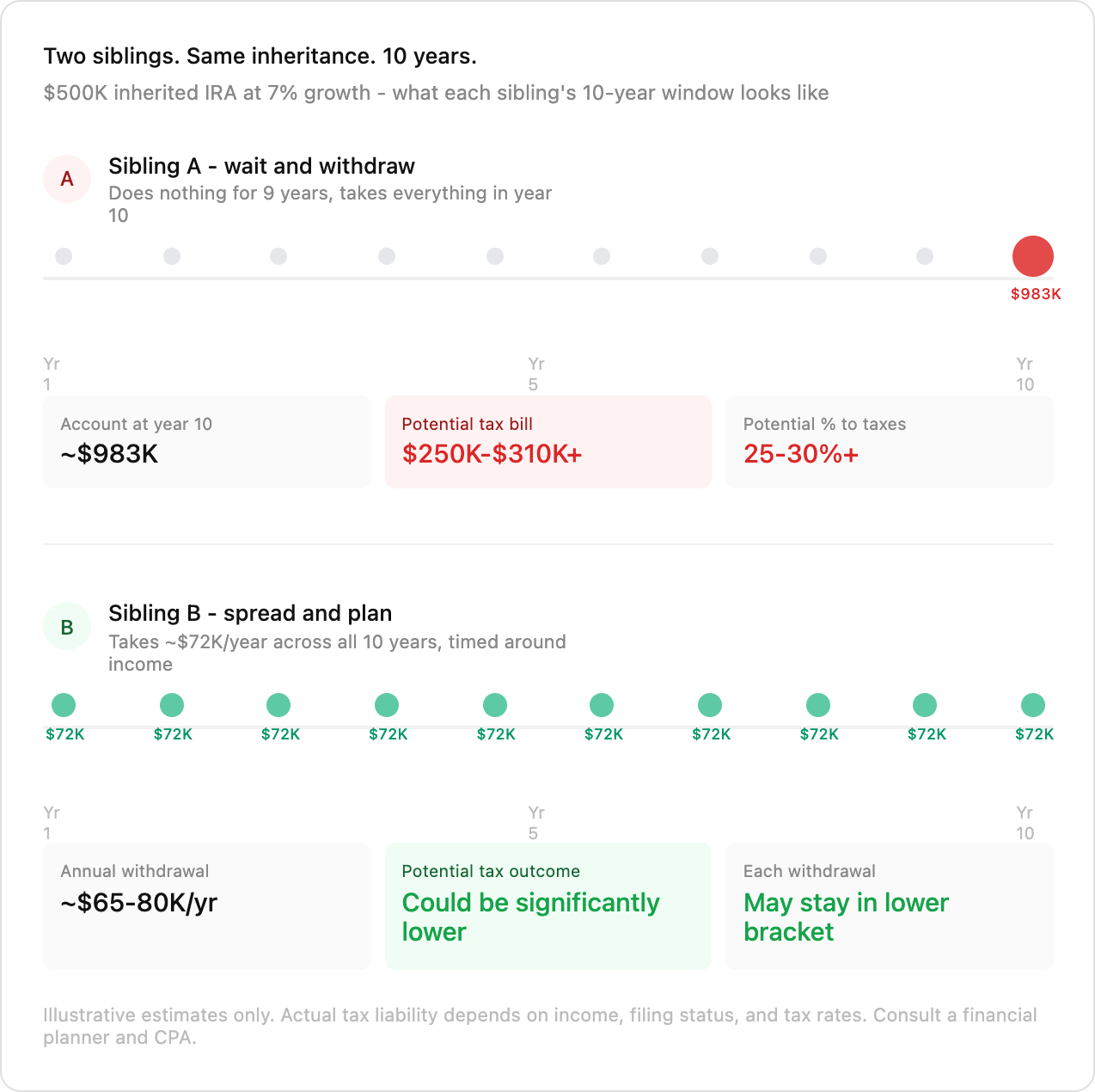

Here’s the pattern we see constantly: a beneficiary inherits an IRA, lets it sit and grow for nine years, then withdraws the entire balance in year 10. On the surface it sounds smart - maximize the tax-deferred growth, delay the tax hit as long as possible.

The math often tells a different story.

Inherit a $500,000 IRA at age 40. At 7% annual growth, that account may be worth close to $983,000 by year 10. Withdraw $983,000 in a single year - stacked on top of your regular income - and the federal tax liability alone could reach $250,000 to $310,000 or more, depending on your situation. That’s potentially 25-30% of the entire inherited account gone in one year.

Not because you made a bad decision. Because nobody told you there was a better approach.

There’s also an important nuance that most people miss entirely. If the original account owner had already passed their Required Beginning Date - meaning they were already taking required minimum distributions - you are generally required to take annual distributions in years 1 through 9 and empty the account by year 10. If they hadn’t yet started RMDs, the rules are more flexible, and you only need to empty the account by the end of year 10. Understanding which situation you’re in shapes everything about how you plan.

Why Spreading Distributions May Change the Outcome

One approach that many financial planners use as a starting point: rather than concentrating the tax hit in year 10, consider spreading withdrawals across all 10 years.

Instead of pulling $983,000 in a single year, taking roughly $65,000 to $80,000 annually may mean each distribution lands in a lower tax bracket, your total tax liability is spread across a decade, and the overall amount you pay to the IRS could be significantly lower. This isn’t a guarantee - your specific tax situation, income, and bracket each year will determine the actual outcome - but for many beneficiaries, the difference is substantial.

This is where your current income trajectory matters as much as the account itself. Many people inherit in their 40s or 50s, during peak earning years. Adding $65,000 to $80,000 of distributions on top of a high salary can push every dollar of that distribution into the 32% or 35% bracket. A thoughtful approach accounts for where your income is headed, not just where it is today.

If you expect to retire in year 6, for example, your final four years inside the 10-year window may be your best opportunity for larger distributions. Income may drop. Tax brackets may open up. The 10-year window isn’t just a distribution deadline - it’s a tax planning window, if you treat it that way.

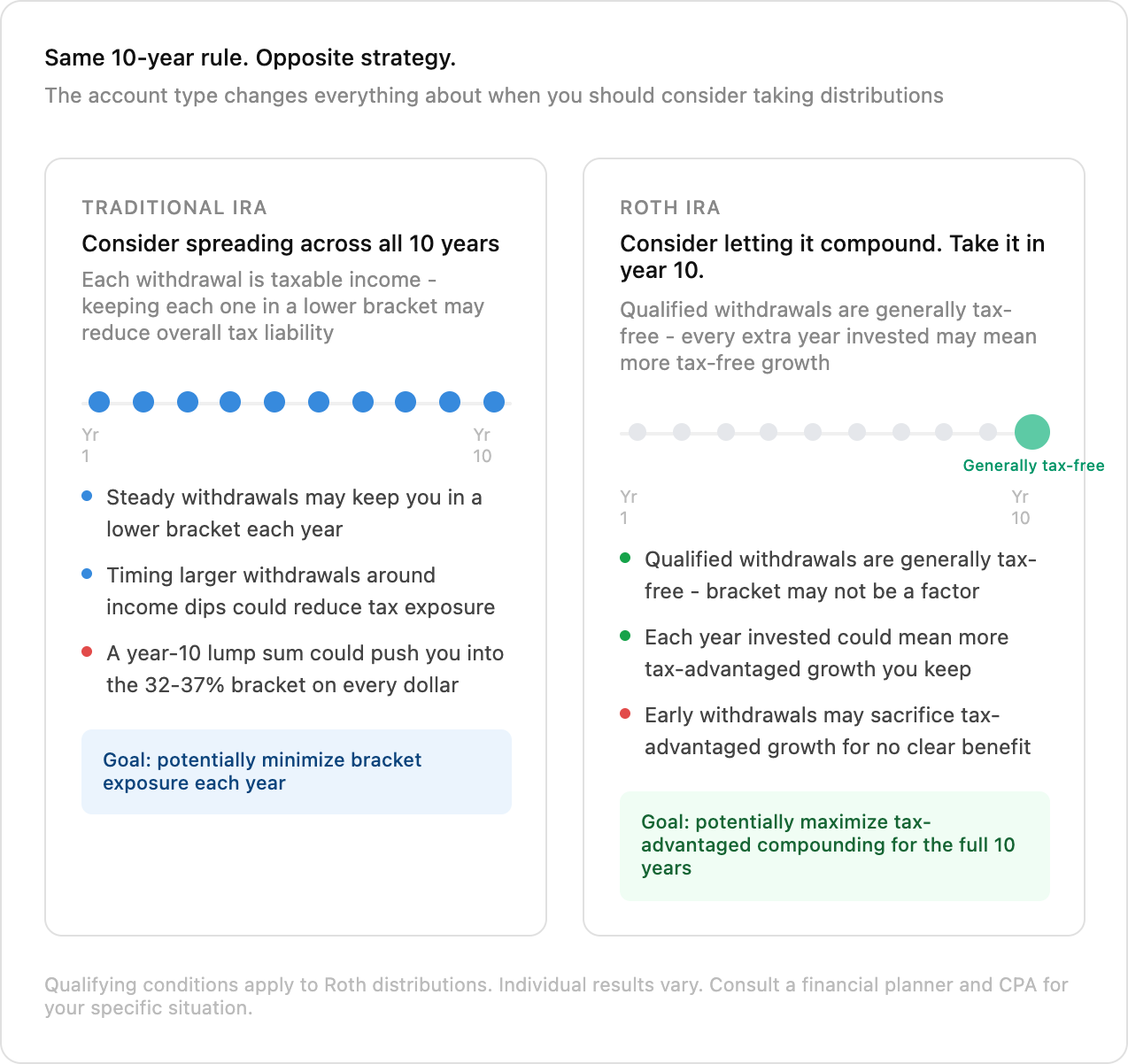

The Roth Inherited IRA - Where the Strategy Flips

If you inherit a Roth IRA, the 10-year rule generally still applies. But the approach many financial planners recommend is the near-opposite of a traditional inherited IRA.

Because Roth distributions are generally tax-free to the beneficiary (qualifying conditions apply), there’s typically little reason to take distributions early. The common approach is to let the account compound for the full 10 years and take the entire balance in year 10 - tax-free. Every year you leave it invested is another year of tax-free growth you’d be giving up by withdrawing early.

Same 10-year rule. Completely different strategy. This distinction alone is worth knowing if you’ve inherited - or expect to inherit - a Roth account.

What We See Most Often

In working with clients through inherited IRA situations, a few patterns come up repeatedly. Beneficiaries who do nothing for years and face a large unexpected tax bill in year 10. Beneficiaries who don’t account for their own income when timing distributions. Beneficiaries who don’t realize they’ve inherited a Roth and treat it the same as a traditional IRA. And beneficiaries who don’t bring a tax advisor or financial planner into the conversation until year 9, when the options have narrowed considerably.

The window for planning is the full 10 years. The earlier you map out a strategy, the more flexibility you have.

Bottom Line

An inherited IRA is a meaningful gift. But without a distribution strategy, a significant portion of it may go to the IRS instead of your family.

The SECURE Act requires most non-spouse beneficiaries to empty inherited IRAs within 10 years

If the deceased had started RMDs, annual distributions in years 1-9 are generally required - not just a year-10 withdrawal

A lump-sum withdrawal in year 10 can result in a tax bill of $250,000 or more on a $500,000 inheritance

Spreading distributions across the 10-year window may significantly reduce total taxes paid - the right approach depends on your income, bracket, and retirement timeline

Inherited Roth IRAs generally work in reverse - let it grow and take the balance tax-free in year 10

The 10-year window isn’t a deadline to ignore. It’s one of the more specific and time-sensitive tax planning opportunities that exists - one that opens once and doesn’t reopen. If you’ve inherited an IRA or expect to, this is worth a conversation with a financial planner and a CPA sooner rather than later.

See you next week.

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.

Super important stuff here Fran!

So nuanced but Secure Act certainly changed the thinking. Great read.