Trump Accounts: What Parents with Kids Born Before 2025 Need to Know

A complete guide to what children born before 2025 actually qualify for—and why the window is still open.

Last week a client sent me a quick message: “My son is 4. Did we miss Trump Accounts entirely?”

He’d seen the headlines. $1,000 per newborn. Born after January 1, 2025 only. His son didn’t qualify for the seed.

He assumed that was the whole story.

It wasn’t. I walked him through what his 4-year-old actually had access to. Twenty minutes later, they were ready to open an account this summer.

Here’s what I told him.

What You Got Right

The $1,000 government seed is real. Deposited at birth for children born between January 1, 2025 and December 31, 2028. If your child was born before 2025, they don’t qualify.

You’re right about that.

But that’s where most of the coverage stopped. And that’s where most parents stopped too.

The seed is one piece of an account that’s still fully available to your child. The rest of the story—how it works, who qualifies, what the math actually looks like—didn’t make the headlines.

Here’s what I walked my client through:

How the account works

What his 4-year-old actually qualifies for

Who can fund the account and how much

How to open one today

What the compounding math looks like starting at age 4

How the Account Works

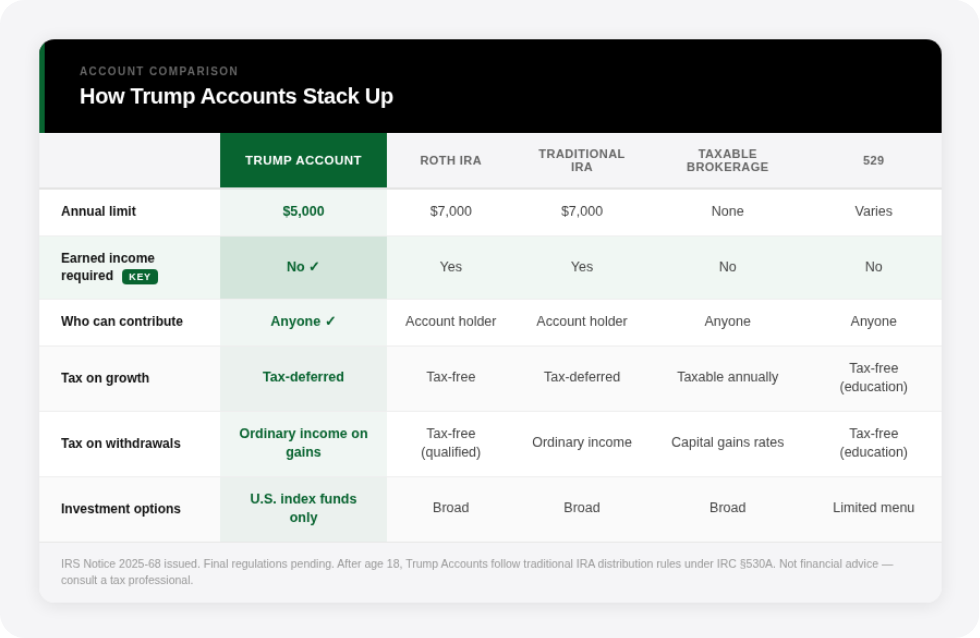

Trump Accounts were created by the One Big Beautiful Bill Act, signed July 4, 2025. The account structure lives in IRC §530A. Contributions open July 4, 2026.

Here’s the tax picture most people don’t have.

Contributions go in with after-tax dollars. Growth is tax-deferred. Here’s what that means at withdrawal:

Contributions (your basis): returned tax-free

Growth: taxed as ordinary income—not capital gains rates, not tax-free like a Roth

Penalty exceptions (education, first home): waive the 10% early withdrawal penalty only—the income tax on growth still applies

The honest take: it’s not as clean as a Roth IRA or a 529. But the reason this account is worth paying attention to comes down to one row in the table below.

Trump Accounts aren’t a replacement for a Roth IRA, a 529, or a taxable brokerage. The investment menu is narrow. The tax treatment isn’t as clean.

But for a child with no earned income and a family who wants to start building early, they’re a meaningful complement—especially once you factor in a planning move available at 18.

More on that at the end.

What Your Child Actually Qualifies For

Michael and Susan Dell are contributing $250 to children age 10 and under, born before 2025, in ZIP codes where the median household income is under $150,000.

Not government money. Doesn’t count toward contribution limits. And it’s mutually exclusive with the $1,000 seed—your child can only receive one or the other.

Kids 11 and older may still qualify if funds remain after initial sign-ups. Any child under 18 can open an account.

Who Can Contribute

No earned income required. That’s the detail most people miss.

A Roth IRA requires the child to have their own income. Trump Accounts don’t. Anyone can contribute—parents, grandparents, relatives, friends, employers, charities.

The annual limit is $5,000 per child, total across all contributors. Employer contributions through cafeteria plans count toward that cap, up to $2,500. The Dell $250 sits outside it entirely—your family can still contribute the full $5,000 in the same year.

How to Open One

File IRS Form 4547 at TrumpAccounts.gov right now. Or include it with your 2025 tax return by April 15—most tax software will have the form.

Accounts go live July 4, 2026. No withdrawals until the child turns 18.

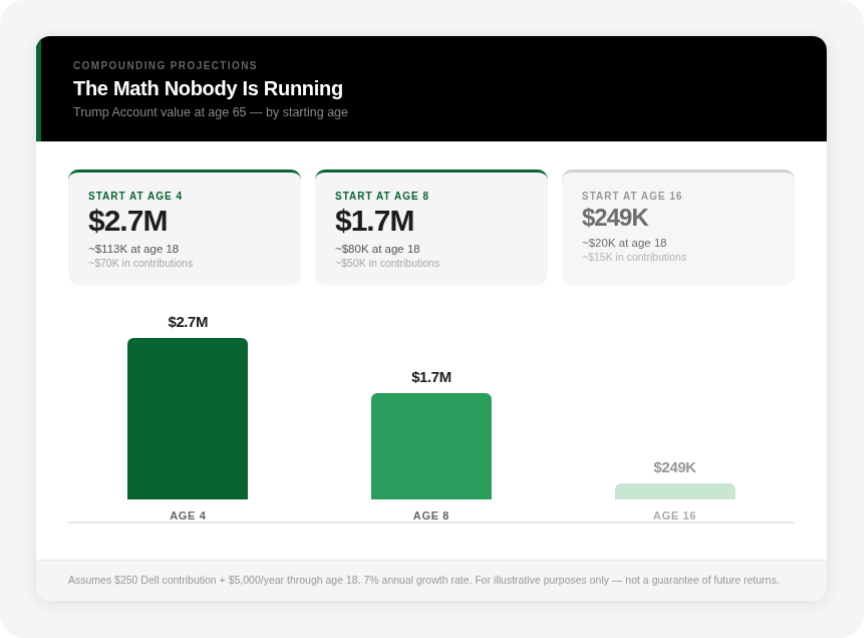

The Math Nobody Is Running

Every projection you’ve seen has been built around a newborn. Here’s what the numbers look like for the kids already in your house:

Starting at 4 isn’t the same as starting at birth. Still a lot better than starting at 16.

One More Move Worth Knowing

As early as 18, account holders can execute a Roth conversion—and it doesn’t require earned income. That path? It doesn’t exist anywhere else.

I covered the full mechanics and the math in this thread: Trump to Roth Conversion Strategy.

That’s it.

My client’s son isn’t getting the $1,000 seed.

But he’s getting an account opened this summer, a $250 Dell contribution, and a family maxing $5,000 a year starting at age 4.

That’s not missing out. That’s a head start.

The parents who sort this out in 2026 — while most are still checked out after the seed headline — are the ones making the decision with full information. Not the ones letting the confusion make it for them.

That window is open right now.

Thanks for reading. See you next week.

— Ryan

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.