The 10-Year Window Nobody Talks About

The math nobody shows you - and why the first decade is worth more than everything that follows.

I sat down with a friend last week - late 20s, good job, smart person - and asked why they still hadn’t started investing.

The answer? They weren’t ready to be a “full grown adult” yet. Still enjoying life. Plenty of time for all that later.

I didn’t lecture them. I just pulled up a simple example - two people, two starting ages, one number at the end. I showed them the math between starting at 22 versus waiting until 32.

They stared at it for a second and said: “Why has nobody ever shown me this before?”

That’s the question I keep coming back to.

Let’s dig in ↓

The Numbers

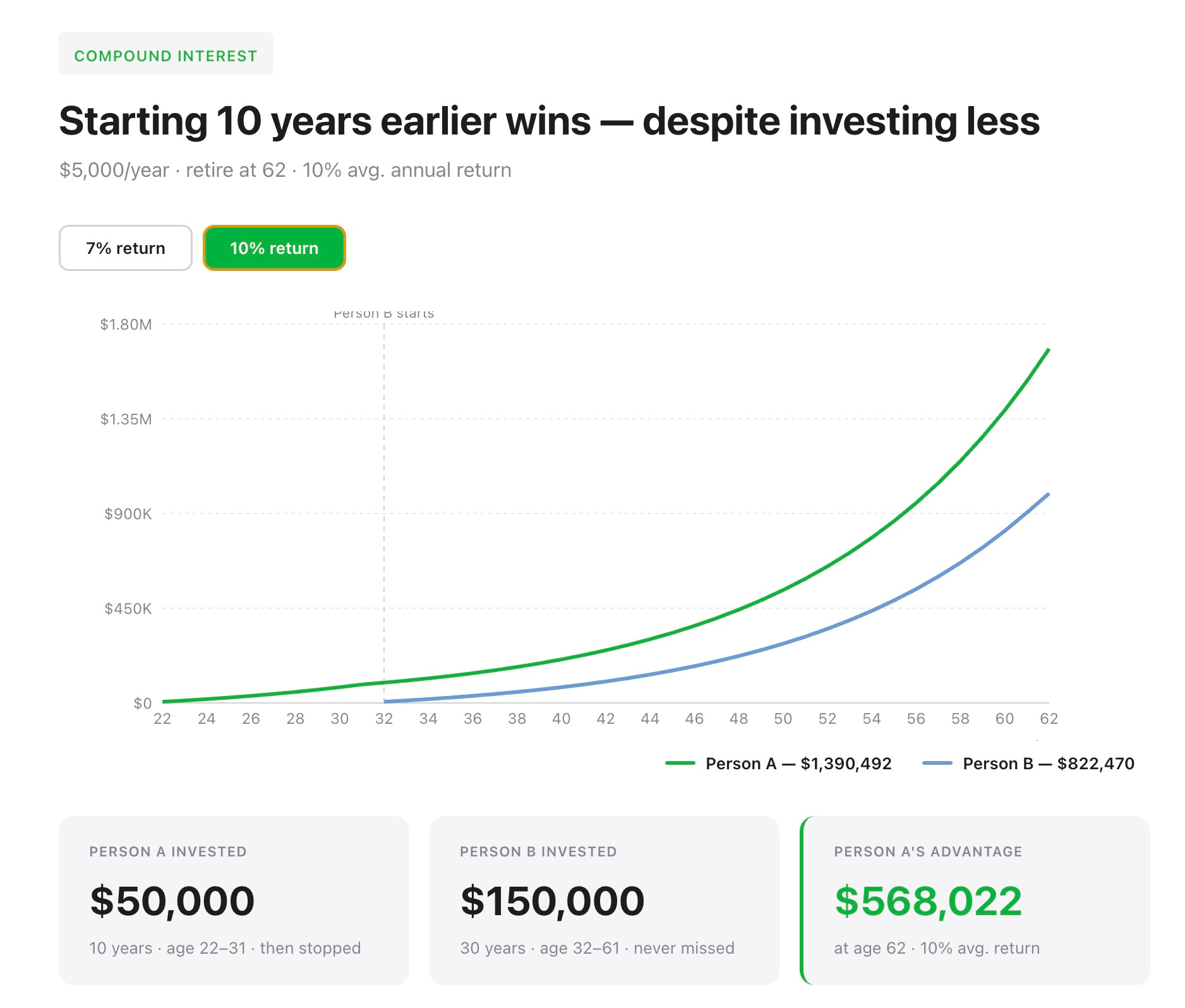

Take two people. Same index fund. Same average annual return. Neither touches the money until age 62. The only difference is when they started.

Person A starts at 22. Invests $5,000 per year for 10 years. Stops completely at 32. Total invested: $50,000.

Person B starts at 32. Invests $5,000 per year for 30 straight years. Never misses a contribution. Total invested: $150,000.

Person B invested three times more money.

Person A still wins. It isn’t close.

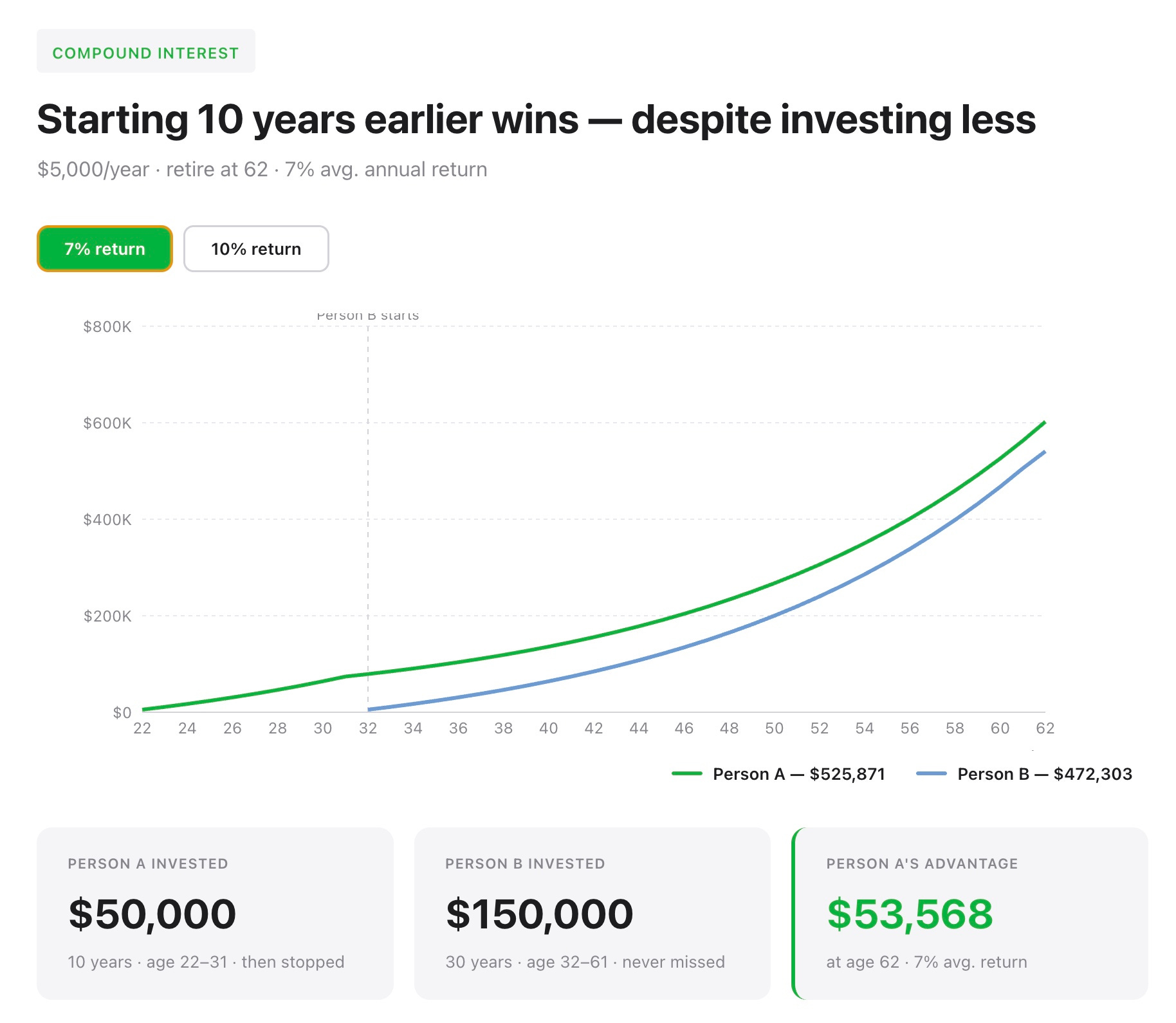

At 10% average returns, Person A finishes with $1,390,492. Person B finishes with $822,470 - a gap of roughly $568,000 in favor of the person who stopped investing decades earlier and put in $100,000 less. At a conservative 7%, the outcome is closer, yet the same: Person A has $525,871, Person B has $472,303.

Why This Happens

Person A’s money had a 10-year head start. Those early dollars compounded for 40 years. By the time Person B made their first contribution, Person A had already built a structural advantage that 30 years of disciplined catch-up couldn’t overcome.

A dollar invested at 22 has 40 years to compound. A dollar invested at 32 has 30. That 10-year gap in the exponent - not the contribution amount - decides the outcome.

And to fully close that gap? Person B would need to contribute approximately $8,500 per year instead of $5,000. That’s 70% more, every single year, for 30 years - just to tie.

You cannot buy back time. You can only pay a steep premium to approximate it.

What If You’re Already “Behind”?

Here’s where I want to be direct with anyone reading this who is 35, 38, or 42 and feeling the weight of those numbers.

You are not stuck being Person B.

If you’re 38 and starting today, your money has 24 years to compound before 62. That’s still a long runway. What changes is the required contribution - which is why income growth matters. Not to inflate your lifestyle, but to fund the catch-up investing that earlier-you didn’t do.

A few ways to get started today:

Open a Roth IRA/Brokerage - takes about 10 minutes

Enroll in your employer’s 401(k) and contribute at least enough to get the match

Set up an automatic monthly contribution - even $200/month is a start

If your employer doesn’t offer a 401(k), a traditional IRA works the same way

The Most Valuable Thing You Can Do With This Math

The most powerful use of this illustration isn’t for yourself. It’s for someone young in your life - a kid, a younger sibling, a new grad - who still has those early years in front of them.

Most 22-year-olds have never seen this math. When you show them Person A and Person B side by side, something clicks that no amount of generic financial advice ever achieves.

The window Person A used is still open for a lot of people reading this. And for the people in your life who are just starting out - it’s wide open. That’s worth a conversation.

The Bottom Line

Person A invested $50,000 over 10 early years and accumulated $1,390,492 by 62.

Person B invested $150,000 over 30 later years and accumulated $822,470.

The 10-year head start was worth roughly $568,000 more - despite $100,000 less contributed and 30 fewer years of discipline.

Every year of delay requires materially higher future contributions just to produce the same outcome.

Starting imperfectly today beats starting perfectly later - every single time.

The market doesn’t care when it’s convenient. Compounding doesn’t wait for your raise. The only variable you can actually control is when you start.

See you next week.

Whenever you’re ready, there are 2 other ways we can help you:

30-Day Strategy Sprint: Got a specific financial challenge holding you back? In just 30 days, we’ll tackle 1-3 of your biggest money roadblocks and hand you a personalized action plan. Perfect if you want expert guidance without a long-term commitment. Limited spots available.

Ongoing Wealth Partnership: We’ll work with you month after month to slash your taxes, find hidden income opportunities, and build lasting wealth. You set the life goals. We handle the financial strategy to get you there faster.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.