The Mental Math Trick That Changes How You See Every Investment

One formula. Three seconds. A completely different way to think about your money.

Every single week, we hear from people who are doing the right things - investing consistently, making contributions, building the habit. But they have no idea if they’re doing enough. They can’t picture where they’ll actually land in 5, 10, 15, or 20 years. They’re putting money in and hoping the math works out.

That’s not a motivation problem. It’s a visibility problem.

Most people don’t have a mental model for compounding. They see a rate of return - say, 7% - and assume it means something. But they can’t feel it. They can’t picture it. They can’t use it to make a real decision in the real world.

There’s a tool that fixes this. It’s been around for centuries. Most people have never heard of it. And once you learn it, you’ll never look at an interest rate the same way again.

Let’s dig in

The Rule of 72

The formula is as simple as finance gets.

Divide 72 by your annual return rate. The result is how many years it takes your money to double.

72 / rate = years to double.

That’s it. No calculator needed. No spreadsheet. Just the number 72 and whatever return you’re working with.

Here’s what it looks like in practice:

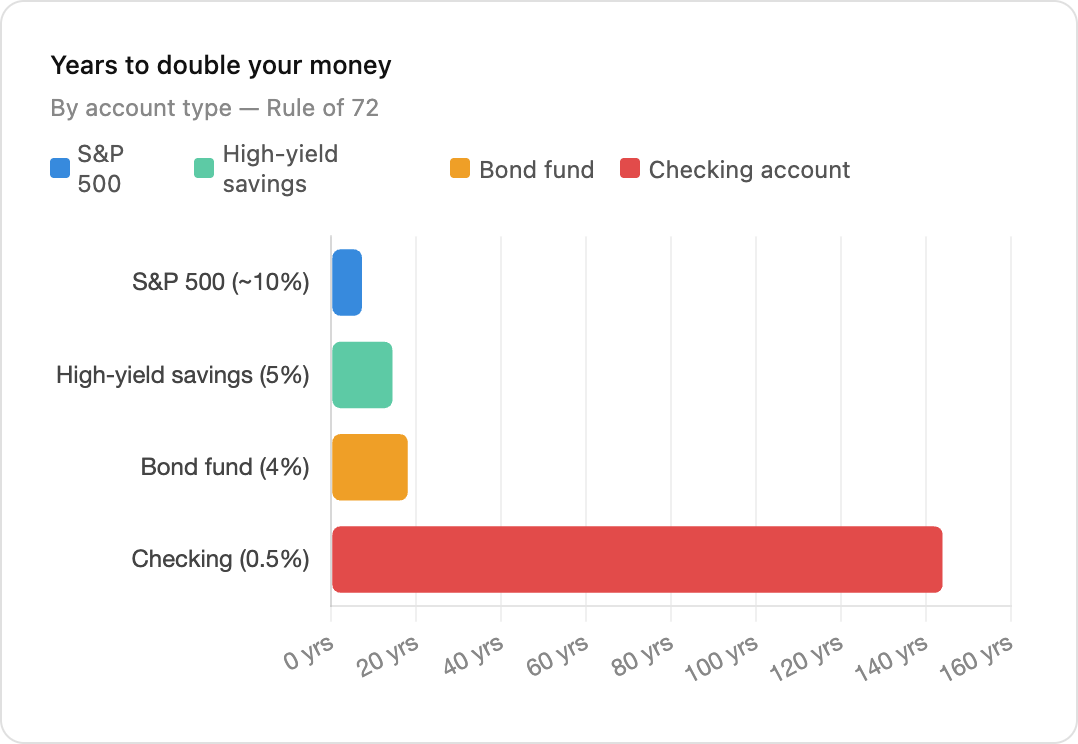

S&P 500 (~10% historical average): 72 / 10 = 7.2 years to double

High-yield savings account (5%): 72 / 5 = 14.4 years to double

Bond fund (~4%): 72 / 4 = 18 years to double

Checking account (0.5%): 72 / 0.5 = 144 years to double

Same money. Same starting point. Wildly different destinations.

When you see it laid out like that, the checking account number doesn’t feel like a conservative choice. It feels like a choice to never double your money in your lifetime.

How to Reverse It

Here’s where the Rule of 72 gets genuinely useful as a planning tool.

Most people set financial goals the wrong way. They say, “I want to retire with $3 million,” without ever asking what return rate they need to get there. The goal sits in the future like a vague hope. There’s no bridge between where you are and where you want to be.

The Rule of 72 lets you build that bridge.

Want to double your money in 10 years? 72 / 10 = 7.2% annual return needed. Now you have a target, not a wish. You can look at your actual portfolio and ask whether it’s built to deliver 7.2%. You can have a real conversation with an advisor about whether your current allocation gets you there.

Want to double in 6 years? You need 12%. That’s aggressive - it’s possible, but it carries real risk. Knowing that in advance means you’re making an intentional tradeoff, not stumbling into one.

This is the difference between passive financial hope and active financial planning.

The Inflation Flip

The Rule of 72 doesn’t just apply to investment returns. It applies to anything that compounds - including the things working against you.

Take inflation. When inflation runs at 6%, your purchasing power doesn’t just slowly erode. It gets cut in half in 12 years. 72 / 6 = 12.

That means the $100,000 sitting in your savings account today buys roughly $50,000 worth of goods and services in 12 years - in real terms. The account balance didn’t change. But what it can actually do in your life did.

This is why holding large amounts of cash during high-inflation periods is one of the most expensive decisions a high earner can make. It doesn’t feel risky. There’s no volatility, no red numbers on a screen. But the math is working against you every single year in a way most people never stop to calculate.

The Rule of 72 makes the invisible visible. Inflation isn’t an abstraction anymore. It’s a number, with a timeline, and a consequence.

The Cousins Nobody Talks About

The Rule of 72 has two less famous relatives worth knowing.

The Rule of 114 tells you how long it takes to triple your money. The Rule of 144 tells you how long it takes to quadruple it.

At a 10% annual return:

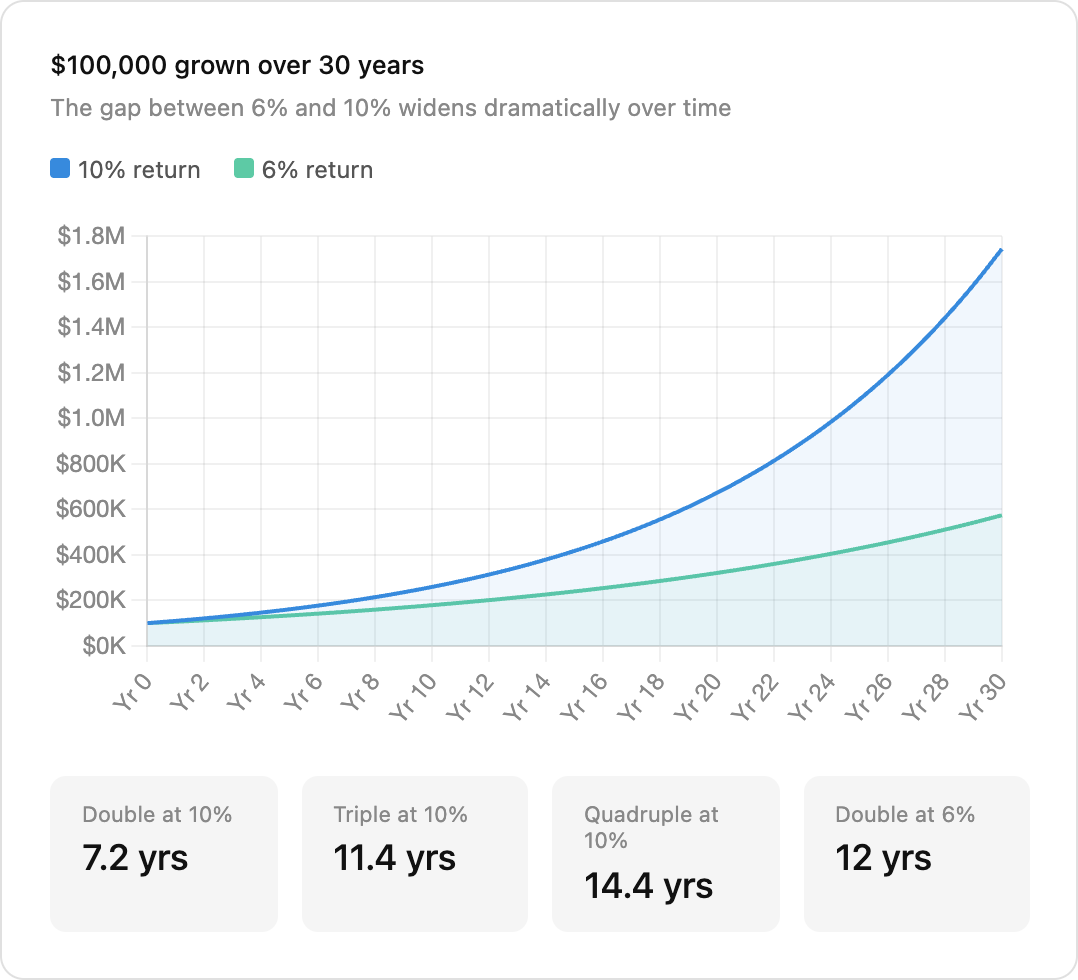

Double: 72 / 10 = 7.2 years

Triple: 114 / 10 = 11.4 years

Quadruple: 144 / 10 = 14.4 years

What this reveals is how compounding accelerates. Your money doesn’t grow in a straight line - it bends. The first doubling takes 7.2 years. The second doubling? Also 7.2 years. But now you’re working with twice as much, so the dollar gains are dramatically larger.

The later years aren’t where you wait for the payoff. They’re where the payoff actually lives.

The Bigger Lesson: Small Differences Are Enormous

This is what the Rule of 72 is really teaching you.

The gap between a 6% return and a 10% return doesn’t sound like much. Four percentage points. Less than half a percentage point per month. But in doubling time, it’s the difference between 12 years and 7.2 years. On a 30-year timeline, that 4% difference doesn’t add a little more wealth. It produces a completely different financial life.

I see this constantly with clients who are obsessively focused on cutting expenses - tracking every subscription, optimizing every grocery run - while sitting in cash or in a savings account earning 4%. They’re trying to win a $200-a-month game while leaving a 7.2-year doubling cycle on the table.

That’s not a dig at frugality. Frugality matters. But it has to be paired with return rate awareness. You cannot save your way to the kind of wealth that creates real freedom. You have to grow your way there. And growing requires understanding that the difference between a 6% return and a 10% return isn’t 4%. It’s time. And time is the one variable you can’t manufacture more of.

How to Apply This Starting Today

Run every account you own through the rule. Your 401(k), your brokerage, your savings account. How long until each one doubles? The results will quickly show you where your money is working and where it’s sitting idle.

Then reverse it for your goals. Pick a target and a timeline, and figure out what return rate you actually need. That number becomes a filter for every investment decision you make - not a vague hope, but a real benchmark.

That said, rate of return isn’t the whole story. Investments exist to support the life you’re building - not the other way around. A 10% return means nothing if the portfolio is keeping you up at night, or if it’s not structured around what you actually need your money to do. The Rule of 72 is a lens for clarity, not a scorecard. The goal is a plan where your investments and your life are pulling in the same direction.

Bottom Line

The Rule of 72 is simple enough to do in your head and powerful enough to change how you see every account you own.

72 / your return rate = years to double your money

72 / your target years = the return rate you need to hit your goal

72 / inflation rate = years until your purchasing power gets cut in half

But the deeper lesson isn’t the formula. It’s what the formula reveals: small differences in return rate, compounded over time, produce outcomes that look nothing alike. The difference between 6% and 10% isn’t incremental. It’s transformational.

Just don’t lose sight of why the math matters. Investments aren’t the goal - they’re the engine. They exist to fund the life you’re designing, and they work best when they’re built around a plan, not chased in isolation. The number you’re trying to double isn’t just a portfolio balance. It’s your freedom, your options, your time.

Start with your own accounts. Run the numbers. Then make sure the strategy behind them is pointed at something that actually matters to you.

Because the goal was never just to have more money. It was to have a life worth building toward.

See you next week.

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.

This Rule of 72 piece is pure gold simple, sticky, and instantly useful for teens. Keep these gems coming.