The $83,000 Mistake Generous Parents Make Without Knowing It

How gifting appreciated stock may transfer your tax liability along with your generosity - and what to do instead.

We sit across from generous parents all the time. They’ve built wealth, their kids could use some help, and they want to do something meaningful. So they gift appreciated stock - something that’s grown substantially over the years - because it feels like a real, tangible transfer of wealth.

What they may not realize is that along with the stock, they’re also transferring their original cost basis. And everything that comes with it.

This week we’re breaking down one of the most overlooked provisions in the tax code - the stepped-up basis - and why the timing of how you transfer appreciated assets may matter as much as the decision to transfer them at all.

One important note before we dig in: this is a tax optimization framework for families who are in a position to be patient. If your kids need the money today and you can help them, you help them - and whoever takes the tax hit takes the tax hit. That’s the right call. What follows is for situations where everyone is financially okay and the goal is to pass wealth as efficiently as possible.

Let’s dig in:

Cost Basis: The Number That Determines Your Tax Bill

When you buy a security, the price you pay becomes your cost basis. When you sell, you may owe capital gains tax on the difference between what you paid and what you received.

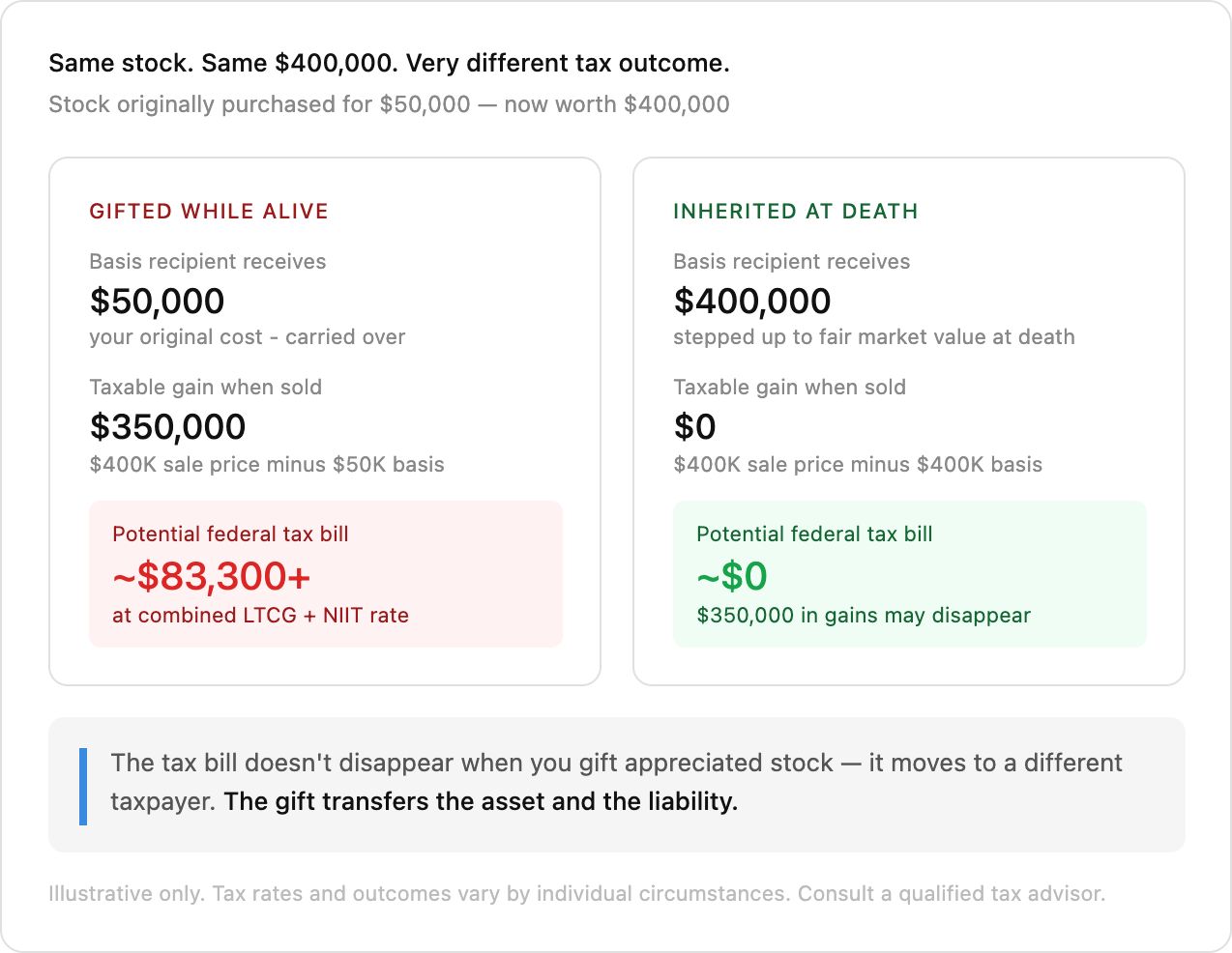

Stock purchased for $50,000, now worth $400,000, has $350,000 in embedded gains. If sold today at the long-term capital gains rate plus the net investment income tax - a combined rate that can reach 23.8% for high earners - the potential federal tax bill on that gain could reach approximately $83,300.

That number doesn’t disappear when you give the stock away. It goes with whoever ends up holding it.

What Happens When You Gift Appreciated Stock While Alive

When you gift appreciated stock to a family member during your lifetime, the recipient generally receives your original cost basis - known as carryover basis.

The stock you bought for $50,000 and gifted at $400,000? Your child’s basis is generally still $50,000. When they sell, they may owe tax on the full $350,000 gain - the same tax bill that would have existed in your hands, now sitting in theirs.

This is the pattern we see regularly. A parent gifts appreciated stock with genuine generosity, believing they’re transferring wealth. What they may actually be transferring is the tax liability embedded in that position.

The wealth transferred is real. But so is the bill that comes with it.

What Happens When Appreciated Stock Is Inherited Instead

Here’s where the tax code does something that surprises most people the first time they see it.

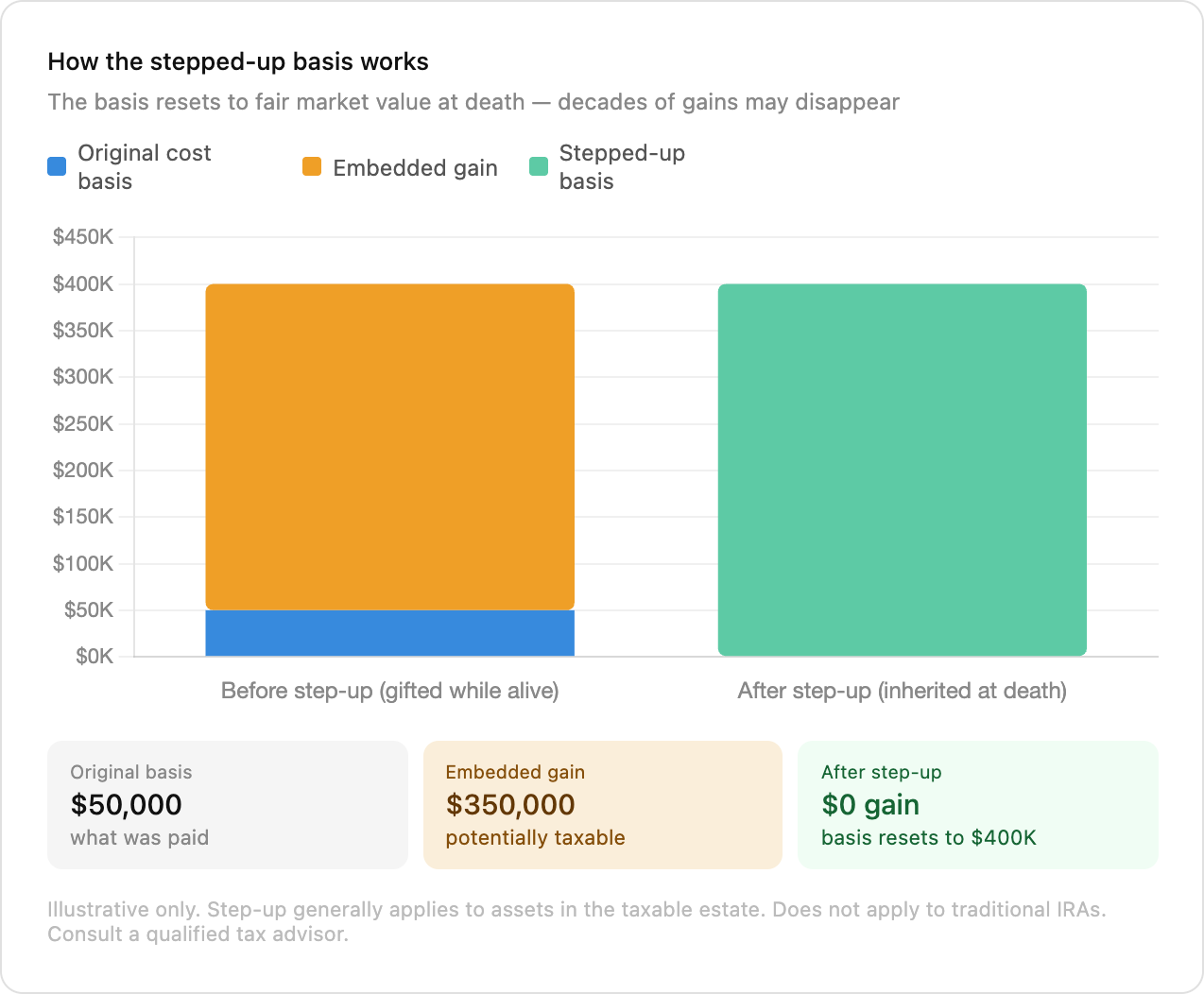

When a beneficiary inherits appreciated stock, the cost basis generally resets to the fair market value on the date of death. This is the stepped-up basis. That $50,000 position, now worth $400,000, generally steps up to $400,000 at the time of inheritance.

Sell it the next day? The potential federal capital gains tax on that $350,000 in gains may be zero.

Same stock. Same $400,000. Same $350,000 in embedded appreciation. Gifted while alive: heir carries a $50,000 basis and may face an $83,000+ federal tax bill when they sell. Inherited at death: basis generally resets to $400,000 and the gain may disappear entirely.

The stepped-up basis is one of the most powerful provisions in the tax code. It’s also completely legal. It exists because Congress determined that taxing unrealized gains at death would be administratively complex and disruptive to families and businesses. The result: decades of appreciation may pass to the next generation with no federal capital gains tax at all.

The Exception That Changes Everything: Retirement Accounts

This is the nuance that most conversations about the step-up miss - and it may be the most important part.

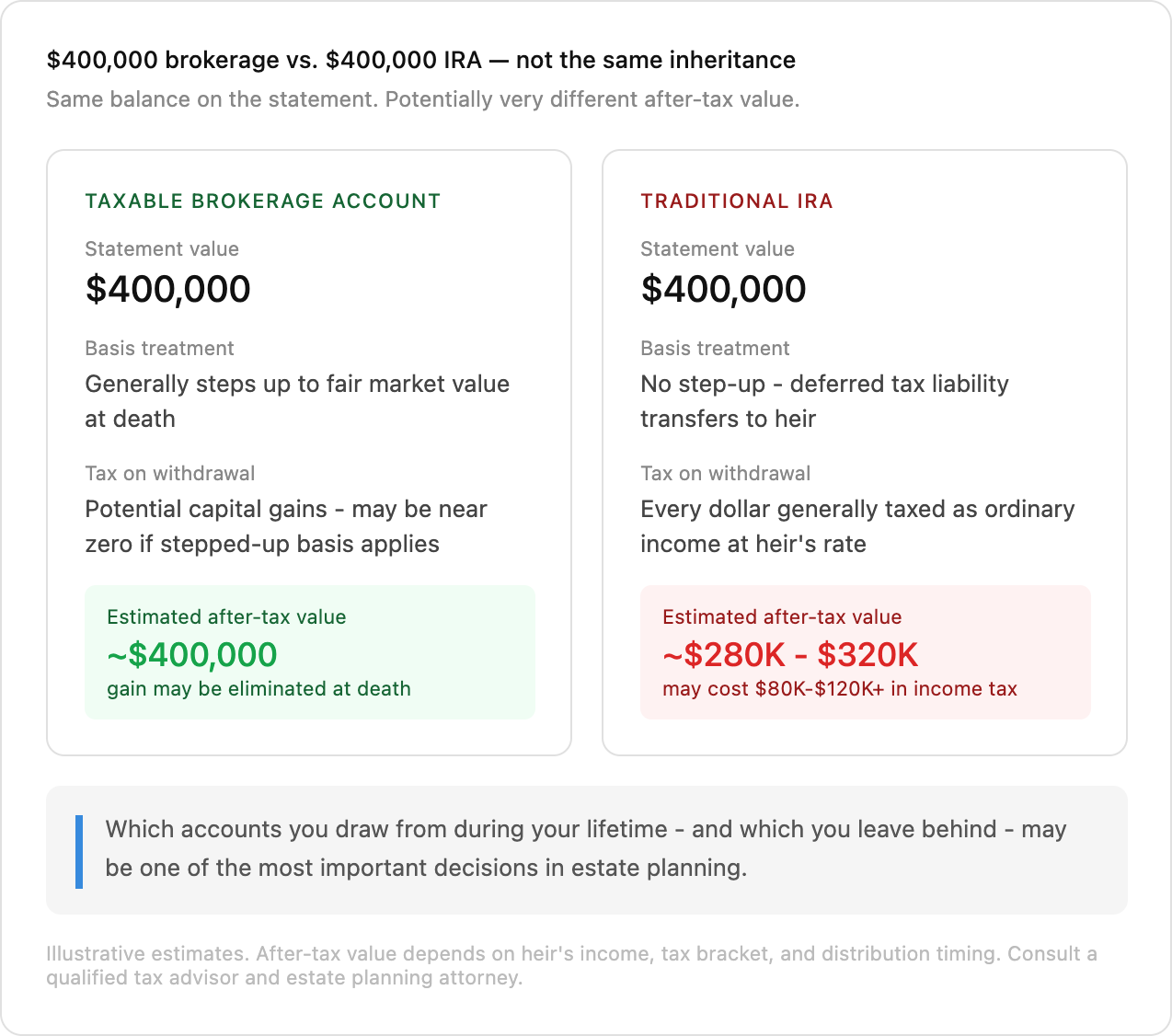

The stepped-up basis generally does not apply to traditional IRAs and retirement accounts.

When you inherit a traditional IRA, every dollar you withdraw is generally taxed as ordinary income - not at capital gains rates, but at your income tax rate. There is no basis reset. There is no step-up. The deferred tax liability that existed in the account while your parent was alive generally transfers directly to you as the beneficiary.

This means a $400,000 taxable brokerage account and a $400,000 traditional IRA are not the same inheritance - not even close. The brokerage account may pass with little or no federal capital gains tax if it holds appreciated securities. The IRA may cost the heir $80,000 to $120,000 or more in income tax over the distribution period, depending on their bracket and how distributions are timed.

Same dollar amount on the statement. Potentially very different after-tax value in your hands.

The Asset Location Decision Most Estate Plans Miss

This distinction changes how thoughtful families think about which assets live where.

The conventional wisdom on asset location focuses on current tax efficiency: hold tax-inefficient assets like bonds and REITs inside retirement accounts, and hold tax-efficient assets like index funds and growth stocks in taxable accounts. That logic holds during accumulation.

But there’s an estate planning layer that often gets missed entirely. Assets with large embedded gains in taxable accounts may be ideal candidates to pass as an inheritance - because the stepped-up basis may eliminate the gain entirely at death. Those same assets gifted while alive transfer the gain to the recipient.

IRA assets, by contrast, pass with the full ordinary income tax liability intact. A Roth IRA is a meaningful exception - qualified Roth distributions are generally tax-free to heirs - which is one of many reasons Roth conversion strategy matters in estate planning contexts.

The question worth asking: which accounts am I drawing from during my lifetime, and which am I leaving behind? The answer may have significant implications for what heirs actually receive.

One Important Caveat on Larger Estates

The step-up generally applies to assets in the taxable estate. For estates above the federal exemption - $13.99 million per individual and approximately $27.98 million per couple in 2026 - federal estate tax may apply at 40% on amounts above the threshold.

At that level, the interaction between estate tax and the stepped-up basis becomes more complex, and the right strategy may look very different. If your estate approaches those thresholds, this is a conversation that warrants dedicated attention from an estate planning attorney and a CPA - the stakes are significant enough that general frameworks may not be sufficient.

For the majority of families below those thresholds, the stepped-up basis remains one of the most accessible and meaningful tax planning tools available.

The Practical Takeaway

If you’re in a position to be generous and want to transfer wealth to your children efficiently, the sequencing matters.

Consider gifting cash rather than appreciated stock during your lifetime. The recipient gets the full value without inheriting your embedded tax liability. Leave appreciated positions in taxable accounts as part of the inheritance - where the basis may reset at death and the gain may disappear. Draw from retirement accounts during your lifetime rather than leaving them as the primary inheritance, since heirs will generally owe ordinary income tax on every dollar they withdraw.

None of this requires exotic strategies or complex structures. It requires knowing which assets carry embedded tax liabilities and being intentional about when and how they transfer.

Bottom Line

Most people think estate planning is about wills and trusts. It’s also about which account holds which asset - and what that decision may cost heirs in taxes.

Gifting appreciated stock while alive generally transfers your original cost basis to the recipient - along with the potential tax liability embedded in the position

Inheriting appreciated stock generally resets the basis to fair market value at death - potentially eliminating decades of embedded gains

The stepped-up basis does not apply to traditional IRAs - every dollar inherited from a traditional IRA is generally taxable as ordinary income

A $400K taxable brokerage account and a $400K traditional IRA are not the same inheritance - the after-tax difference may be $80,000 to $120,000 or more

For estates below the federal exemption threshold, the stepped-up basis may be one of the most powerful tax provisions available - and it requires no complex planning to use

If your children need money today and you can help them - help them. The tax hit is manageable and being there when it matters is the point. But if the goal is long-term, tax-efficient wealth transfer, the order and method of how assets pass may matter as much as the assets themselves.

See you next week.

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.