The 401(k) Provision 90% of High Earners Never Check

You've maxed your limit and captured your match—but one hidden mechanic could be costing you thousands.

You’re maxing your 401(k) at $24,500. You’ve captured your employer match. You think you’re done.

And that’s exactly what most financial advice tells you to do.

But here’s what that advice doesn’t mention: Your plan likely has 2-3 hidden provisions worth thousands annually. And one in particular that 90% of high earners overlook completely.

Here’s your 2026 optimization checklist—basic to advanced.

Start With The Foundation

Most optimization begins here. Update your limits and lock in your match.

Move 1: Update Your 2026 Contribution Limits

If you’re under 50, you can contribute $24,500 in 2026 (up from $23,500 in 2025).

If you’re 50-59, add the $7,500 catch-up for a total of $32,000.

If you’re 60-63, you qualify for the enhanced catch-up: $11,250 on top of the base limit. That’s $35,750 total.

If you’re still on autopilot from last year, you’re under-contributing by $1,000 to $2,250 depending on your age.

Log into your plan this week. Update your deferral percentage to capture the full limit. This is the easiest money you’ll make all year.

Move 2: Confirm Your Company Match Formula

Know exactly what your employer contributes. Most common formulas: 50% match on 6% of salary, or 100% match on 3%.

If you earn $300,000 and your employer matches 50% on 6%, that’s $9,000 in free money annually.

Missing it = leaving that $9,000 on the table.

Check your benefits portal for the exact formula. Then adjust your contribution percentage to capture the full match. If the match is 6%, contribute at least 6%. Don’t leave a dollar behind.

The Provision 90% Miss

This is where most high earners lose thousands without knowing it.

Move 3: Check If Your Plan Has a True-Up Provision

This is the hidden mechanic that separates basic contributors from sophisticated optimizers.

Here’s how it works:

Your employer matches 6% of your salary per paycheck. You front-load your contributions and max out by June. July through December? Zero contributions = zero match for those six months.

With a true-up provision, your employer catches you up at year-end. Without it, you forfeit six months of match.

On a $300,000 salary with a 6% match, that’s $9,000 in potential match for the year. Miss half the year? You just left $4,500 on the table.

Ask HR directly: “Does our plan include a true-up provision for employer match?” Or check your Summary Plan Description (SPD).

If yes: Front-load freely. Max early if you want. The true-up protects you.

If no: Spread contributions evenly across all paychecks to maximize match. Calculate your per-paycheck percentage to hit exactly $24,500 by December 31.

This provision alone can be worth $3,000-$6,000 annually for high earners. And most people have never heard of it.

The Moves That Compound

Once the foundation is locked, these three strategies multiply the impact.

Move 4: Review Your Vesting Schedule

Vesting = how long until employer match is 100% yours.

Most plans use cliff vesting (0% until year 3, then 100%) or graded vesting (20% per year over 5 years).

Leave before fully vested = forfeit unvested match.

I’ve seen people leave jobs 2-3 months before full vesting and forfeit $15,000-$25,000. Don’t let that be you.

Check your plan’s vesting timeline. Planning a job change? Time it strategically. If you’re 90 days from full vesting, those 90 days might be worth $20,000.

Move 5: Roth vs Traditional—Don’t Default to All Traditional

Most high earners default to 100% traditional contributions because they’re in the 24%, 32%, or 35% bracket today.

But here’s what I’ve learned after reviewing hundreds of tax situations: Your tax bracket today tells you almost nothing about your optimal strategy.

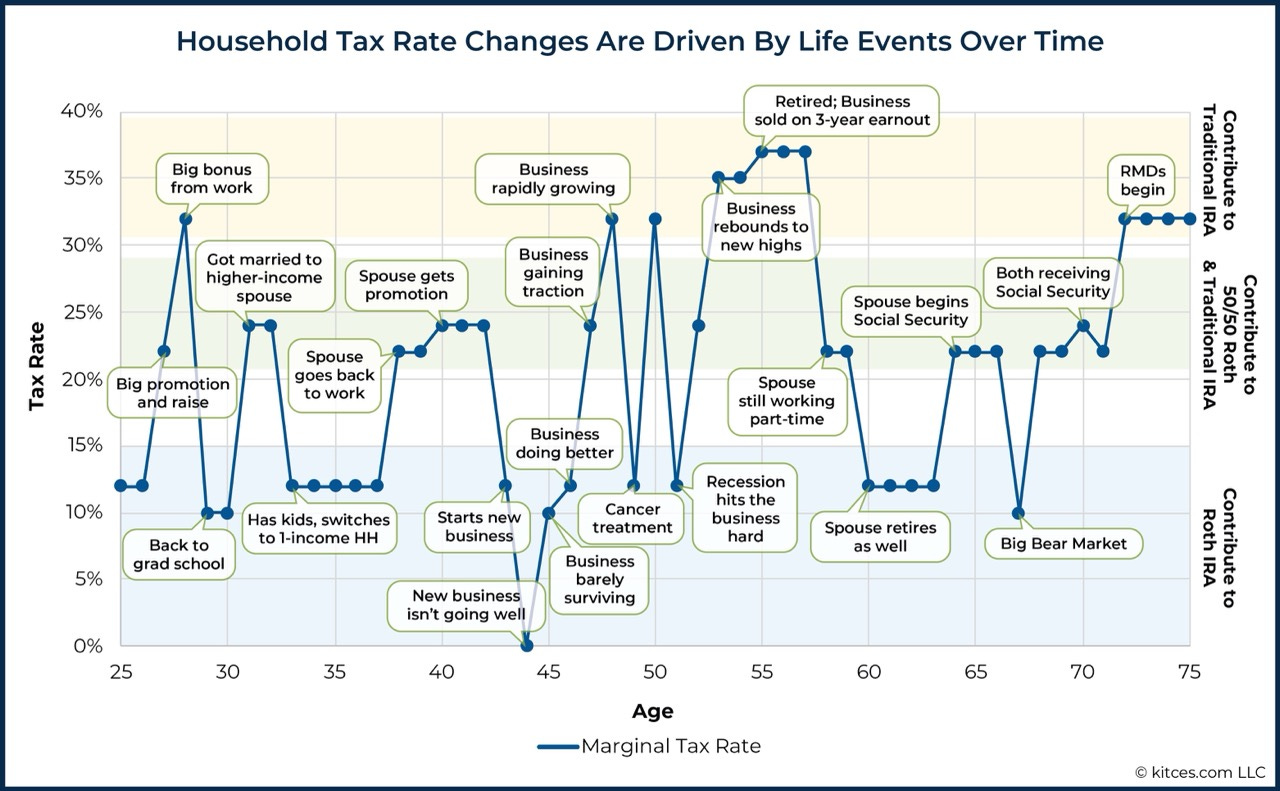

Michael Kitces has a chart I reference constantly. It tracks a hypothetical household’s marginal tax rate from age 25 to 75. The line looks like a heart rate monitor—spikes during peak earning years, drops during career transitions, climbs again with business growth, crashes during recessions, rebounds in retirement.

The pattern shows what we all know but often ignore: Life changes. Income changes. Tax brackets follow.

Big promotion? Your rate jumps. Kid switches to one-income household? It drops. Start a business that struggles? You might hit 10-12% for a year. Business takes off? Back to 32-35%.

Here’s what I’ve seen work with high earners:

When you’re in peak earning years (32-37% brackets), traditional contributions make sense. Take the deduction at high rates now, withdraw later at lower rates.

When you’re in transition years—between jobs, starting a business, taking a sabbatical, or in your first few years of high income before expenses catch up—Roth contributions can be valuable. You’re locking in lower rates that might not last.

When you’re in the middle brackets (22-24%), tax diversification makes sense. Split between traditional and Roth. You’re hedging against future rate changes you can’t predict.

The mistake isn’t choosing wrong. The mistake is setting it once and forgetting it for 10 years.

Your strategy should adapt as your life does.

Move 6: Review Your Investment Selection

Most 401(k)s default you into target date funds. Convenient? Yes. Optimal? Not always.

They’re often too conservative (shifting to bonds too early) and too expensive (0.50%-0.75% expense ratios).

A 0.50% fee difference = $50,000+ over 30 years on a $500,000 balance.

Build your own allocation with low-cost index funds. Most plans offer S&P 500, total market, international, and bond indexes at 0.03%-0.10% expense ratios.

Compare the fees in your plan. The difference compounds faster than you think.

The Advanced Territory

This is high-earner optimization at the next level.

Move 7: After-Tax Contributions + Mega Backdoor Roth

Beyond the $24,500 employee deferral limit, the total contribution limit including employer match is $72,000 for 2026 (~$80,000 if age 50+).

If your plan allows after-tax contributions and in-plan Roth conversions, you can contribute tens of thousands beyond $24,500 and convert it to tax-free growth.

This requires two things:

Your plan allows after-tax contributions (not all do)

Your plan allows in-plan Roth conversions or in-service withdrawals

Check your SPD or ask HR: “Does our plan allow after-tax contributions and in-plan Roth conversions?”

If yes, work with your CPA and financial advisor to set it up properly. This isn’t DIY territory—tax treatment and timing matter.

If available, this strategy can add $30,000-$40,000+ annually in tax-free growth for high earners.

That’s it.

Most high earners think maxing your 401(k) means you’re done optimizing.

But optimization isn’t about how much you contribute. It’s about capturing every provision, timing your taxes right, and knowing which levers exist in your plan.

You don’t have to implement all seven moves this week. Pick one. Start with the foundation. Make sure you’re capturing your 2026 limits and your full match. Then check for true-up. Then layer in the rest.

The difference between basic contributors and sophisticated optimizers isn’t complexity. It’s knowing what to look for.

Now you know.

Thanks for reading. See you next week.

— Ryan

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.

One thing a few team members do is to up the percentage contributions before bonus checks to minimize tax bite from periods of higher income