35 Minutes of Paperwork Could Equal $1.2M More in Retirement

Most advisors steer you toward the wrong retirement account.

Not because they're malicious. Because it's easier for them.

That convenience could be costing you over $1 million in retirement savings. And maybe years of working longer than you need to.

Here's what's happening. You're earning good money on your own. Maybe you're a consultant, freelancer, contractor, or solopreneur. Your CPA mentions setting up a retirement account. They pick a SEP IRA because it's simple to explain and can be set up during tax season.

But there could be a better option sitting right there. One that could put an extra $23,500 in your retirement account every single year.

In this newsletter, you'll discover:

Why the Solo 401k beats SEP IRAs for most self-employed people

The real reason advisors avoid them

How 35 minutes of paperwork creates six-figure lifetime value

The December deadline you can't miss

Your step-by-step action plan to fix this before year-end

Let's fix this once and for all.

Following Old Playbooks

Every self-employed person gets the same tired advice.

"Set up a SEP IRA. It's simple. You can save up to 25% of your income."

Sounds good. Most people nod and move on.

But here's what most people don't know: SEP IRAs only allow employer contributions. When you work alone—as a freelancer, consultant, or contractor—you're both the employee AND the employer.

Solo 401(k)s let you save in both roles. SEP IRAs lock you out of employee savings entirely.

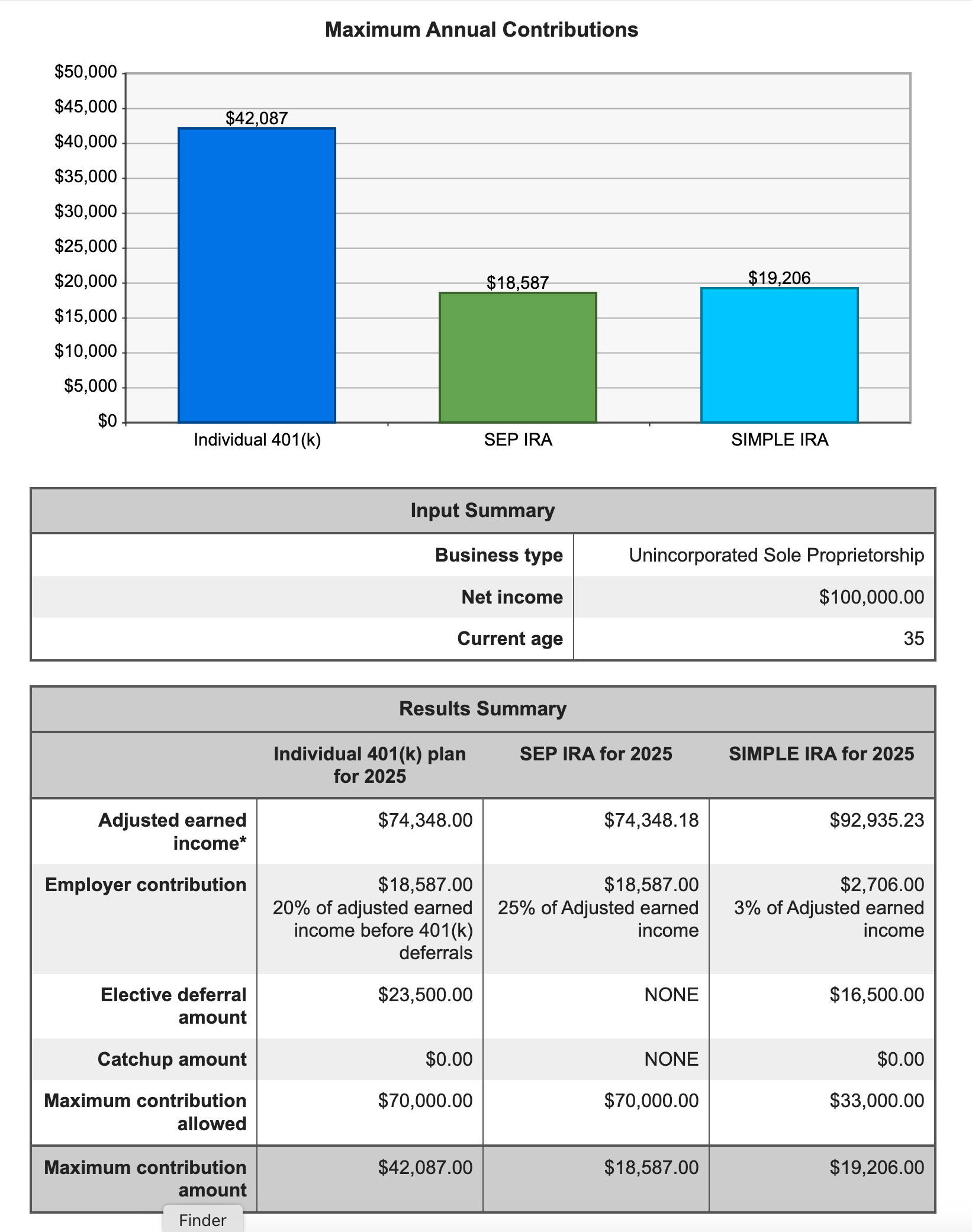

At $100,000 income, a SEP IRA caps you at $18,587. A Solo 401(k)? $42,087.

That's not a small difference. It's a $23,500 gap that grows over time.

And most self-employed people never even hear about the Solo 401k option.

What This Really Costs You

Let's make this hurt a little.

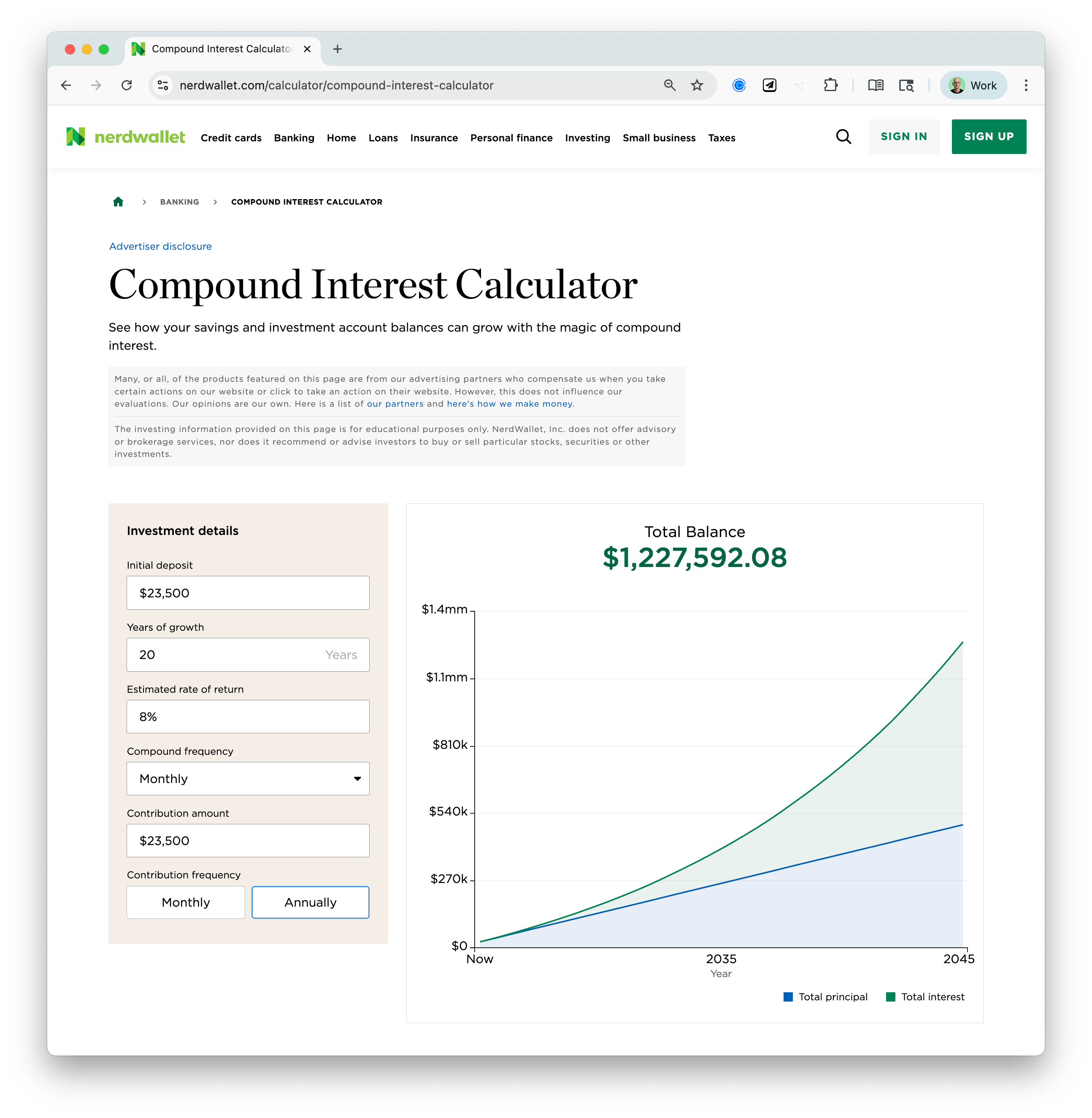

That $23,500 difference doesn't just go away. It grows over time.

Over 20 years at 8% returns, you're looking at $1.2 million less in your retirement account. Not a typo. Over one million dollars.

But the real cost isn't just money. It's time.

With a properly funded Solo 401(k), you could retire years earlier. Or work because you want to, not because your bank account forces you to.

Think about what those extra years of freedom are worth to you.

And once you’ve opened a SEP IRA, most advisors never go back to check if there's a better way.

How the Solo 401(k) Actually Works

Here's the secret weapon hiding in plain sight.

Solo 401(k) lets you save as both employee AND employer.

Employee savings: $23,500 (2025 limit)

Employer savings: Up to 25% of income

SEP IRAs only give you the employer side.

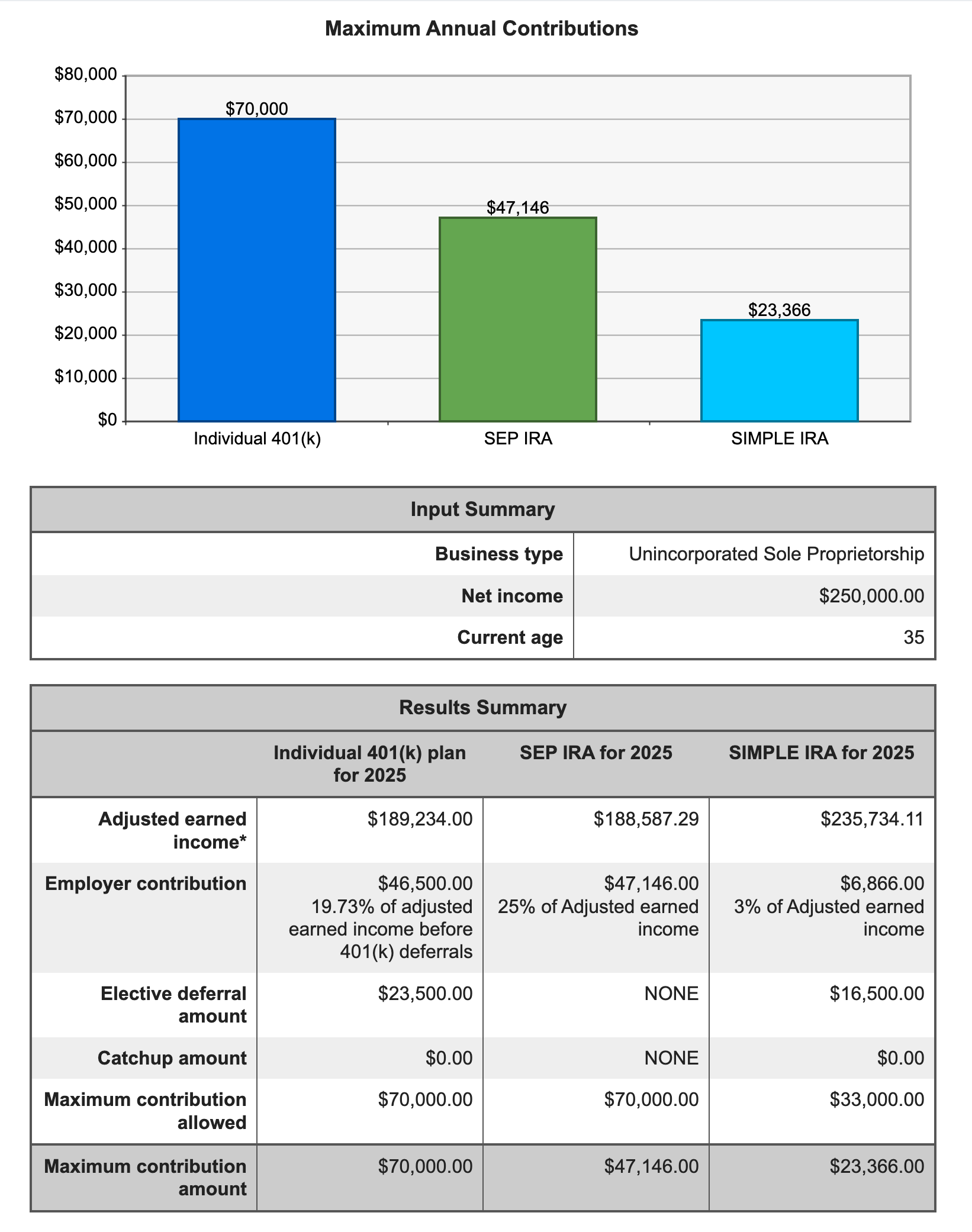

At $250,000 income, you can shelter $70,000 from taxes with a Solo 401(k). That's could be ~$22,400 in taxes savings you keep instead of sending to the IRS at a 32% tax rate.

Plus you get both Traditional and Roth options. SEP IRAs lock you into Traditional only.

This flexibility becomes very helpful as your income and tax situation change.

The Real Reason Advisors Pick SEP IRAs

Solo 401k plans must be set up by December 31st. SEP IRAs can wait until tax time.

Guess when most people think about retirement planning? April. During tax season.

So your advisor picks what they can set up in April. That’s not always what's best for your long-term wealth.

It's not on purpose. It's just how the system works.

But that convenience gap could be costing you six figures over your lifetime.

Your Action Plan: Fix This Before December 31st

Time to stop leaving money on the table.

First, determine if the Solo 401(k) is right for you. Use this Solo 401(k) contribution calculator to see if the Solo 401(k) is a better option than the SEP IRA. Send the report to your advisor to get their perspective.

Then, here's exactly what you need to do:

Call your brokerage (Fidelity, Schwab, Vanguard)

Request Solo 401k application

Complete basic paperwork (15 minutes)

Submit and fund employee portion by December

Calculate profit sharing by April

The December 31st deadline is firm for setup. But once it's set up, you have until tax time to put money in.

Skip this deadline, and you're locked into the worse SEP IRA for another year.

Thirty-five minutes of work. Six-figure lifetime impact.

That's it.

Your advisor will keep picking SEP IRAs because they're easier to explain. Your CPA will keep setting them up because the deadline is flexible.

But you now know what most people never learn: that "simple" choice could be costing you $23,500 every single year.

Here's what's really at stake: In 20 years, you could either have an extra $1.2 million in your account, or you'll be wondering why nobody ever told you there was a better way.

This one insight could mean the difference between retiring early and working into your 70s.

Thirty-five minutes of paperwork is all that stands between you and retiring a decade early.

Thanks for reading. See you next week.

Whenever you're ready, there are 2 other ways we can help you:

30-Day Strategy Sprint: Got a specific financial challenge holding you back? In just 30 days, we'll tackle 1-3 of your biggest money roadblocks and hand you a personalized action plan. Perfect if you want expert guidance without a long-term commitment. Limited spots available.

Ongoing Wealth Partnership: We'll work with you month after month to slash your taxes, find hidden income opportunities, and build lasting wealth. You set the life goals. We handle the financial strategy to get you there faster.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided "as-is" without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.