Your Company Withholds 22% on RSUs. You Might Owe 35%

The tax gap most high earners don't find out about until April - and what to do before it hits.

A friend called me last spring, genuinely confused. He’d had a strong year - good salary, solid bonus, and a significant RSU vest. He felt like he’d done everything right.

Then he got his tax bill.

He owed $8,000 he hadn’t planned for. Not because he spent recklessly. Not because he ignored his finances. Because his company withheld 22% on his vesting shares, and nobody told him that wasn’t enough.

He’s not an outlier. We see this every April.

Let’s dig in ↓

What RSUs Actually Are

RSU stands for Restricted Stock Unit. Your company grants you shares as part of your compensation. You don’t own them yet - they vest over time, typically on a 3 or 4-year schedule.

The most common structure is 4-year graded vesting: 25% of your grant vests each year, creating four predictable tax events. Some companies use a 3-year cliff - nothing for three years, then 100% at once. That single vest can be a massive tax event if you’re not prepared for it. Performance-based RSUs tie vesting to company or individual metrics, which makes the timing harder to predict.

The key thing to understand: the moment your shares vest, the IRS treats the full value as ordinary income. It gets added to your W-2 just like salary. Federal, state, and FICA taxes are all due. And whatever gain or loss you experience after the vest date is a separate capital gains event.

The Withholding Trap

Here’s where it goes wrong for most people.

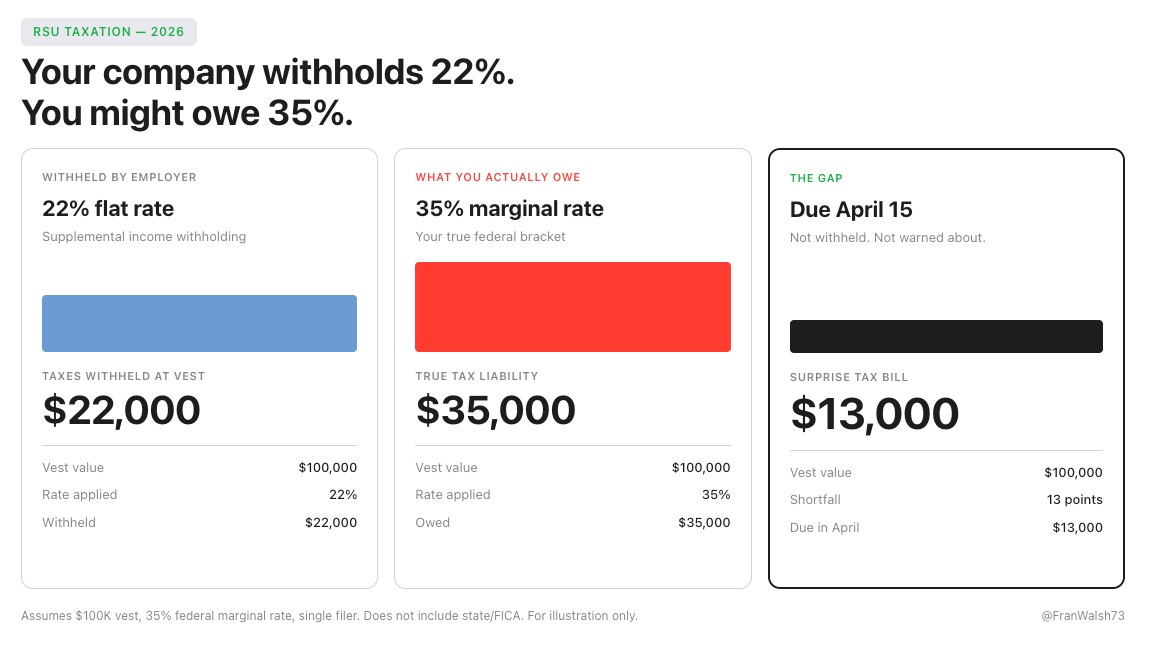

When RSUs vest, your employer withholds taxes on them - but at a flat 22% supplemental income rate. For someone in the 32% or 35% bracket, that gap is significant.

Here’s what it looks like in practice: a $100,000 vest with 22% withheld means $22,000 goes to taxes at the time of vesting. But if your marginal rate is 35%, you actually owe $35,000. That’s a $13,000 shortfall - due April 15.

The problem compounds when RSUs are layered on top of a high base salary. Your salary may already push you into the 32% or 35% bracket before a single share vests. Every dollar of RSU income on top of that is taxed at your marginal rate - not at 22%.

Most people don’t do this math until they’re sitting across from their CPA in March.

The gap can be addressed proactively, but it requires action before the vest happens. Common approaches include increasing W-4 withholding from your salary to cover the difference, making quarterly estimated payments using Form 1040-ES, or using a “sell to cover” election at vest - where enough shares are automatically sold to cover the true tax liability. None of these happen automatically. You have to set them up - ideally with your CPA before your next vest date.

Concentration Risk

The withholding trap is the most immediate problem. Concentration risk is the one that quietly builds over years and then hits all at once.

After 3 or 4 years of vesting at a growing company, it’s common for RSU holders to find that 20-40% of their net worth sits in a single stock. Their employer’s stock. The same company that also pays their salary.

Think about what that means in a bad year. The stock drops, your equity takes a significant hit, and - if the company is struggling - your job security may also be at risk. All three can happen simultaneously.

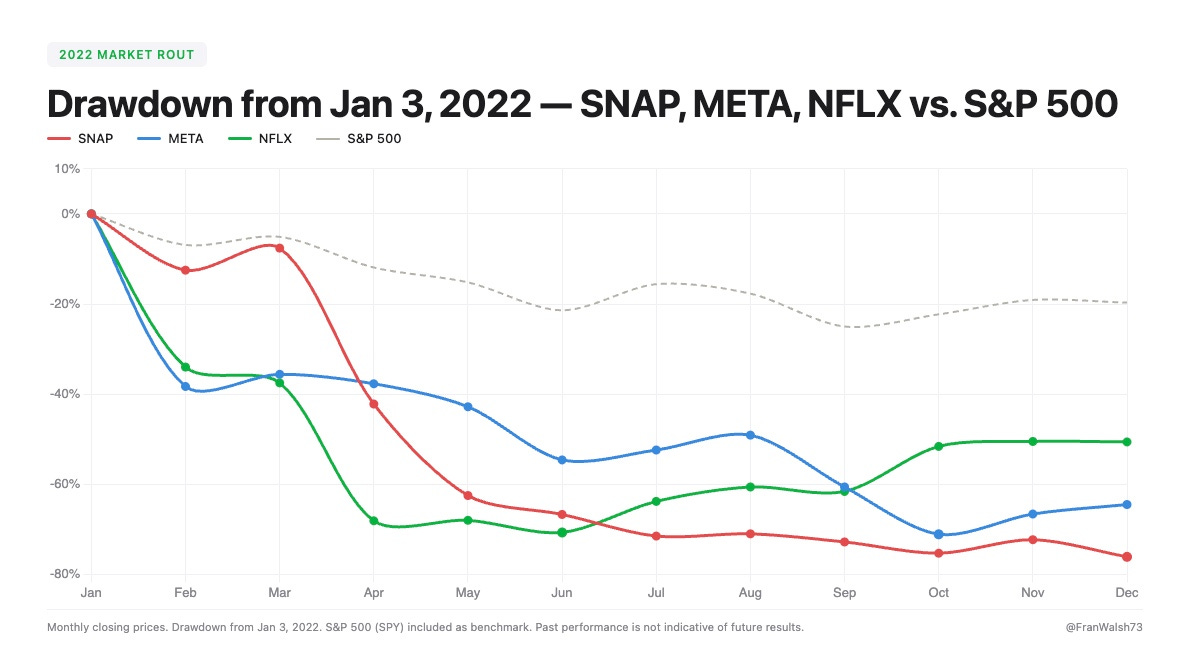

We saw exactly this in 2022. Meta, Snap, and Netflix all dropped 60-70% in a single year. Employees who had held their vested RSUs without diversifying didn’t just lose paper gains - they lost years of accumulated wealth. The people who had been systematically selling and diversifying at each vest were down with the broader market. Not down 60%.

Same grants. Very different outcomes. The only difference was having a plan and executing it.

The approach many financial planners use as a starting point is to sell at vest and diversify. The stock held in your employer is a concentrated bet on a single company - one you already have significant non-financial exposure to through your career. A useful gut check: if you wouldn’t buy that stock with cash today as an outside investor, it’s worth questioning whether holding the RSUs makes sense.

The exception: if you have genuine conviction in the company - not “I work there” conviction, but the kind where you’ve actually analyzed it like an outside investment - and the position stays under 5-10% of your total net worth, holding selectively can make sense. But that threshold matters. Beyond 10%, concentration risk starts to outweigh potential upside for most people.

The LTCG Timing Strategy

This is the piece most RSU holders miss entirely, and it’s where real tax optimization lives.

When your shares vest, their value at that moment becomes your cost basis. That income is already taxed as ordinary income - there’s no avoiding that. But what happens after vest is a different story.

If you hold your vested shares for more than 12 months before selling, any additional gain above your cost basis is taxed at long-term capital gains rates - 0%, 15%, or 20% depending on your income - rather than at your ordinary income rate of up to 37%. For a high earner, that gap is meaningful.

The decision framework is straightforward. Hold beyond 12 months if you have genuine conviction in the stock, the position stays under 10-15% of your net worth, and you can tolerate the volatility of holding a single stock for a year. Don’t hold if you’re already concentrated, if you need the liquidity, or if your conviction is based primarily on the fact that you work there.

The key insight: this is a separate decision from whether to sell at vest. Selling at vest to diversify and holding a small portion for LTCG treatment aren’t mutually exclusive strategies.

The RSU Optimization Checklist

Before your next vest, work through these:

Map your full vesting schedule and identify every upcoming tax event

Calculate your true marginal rate - not the 22% your employer uses

Fix your withholding or set up quarterly estimated payments to cover the gap

Decide your default position on selling vs. holding before the shares vest, not after

If holding beyond vest, track the 12-month clock carefully for LTCG treatment

Keep your employer stock position under 10-15% of total net worth

The Bottom Line

RSUs feel like found money. They’re not. Each vest is a tax event, a concentration decision, and a planning opportunity - all at once.

Your employer withholds 22%. If you’re in the 35% bracket, that gap on a $100,000 vest is $13,000 due in April.

After a few years of vesting, concentration risk becomes the bigger threat - one bad year hits your equity and your income at the same time.

The default is to sell at vest and diversify. Hold selectively only with real conviction and under 10-15% of net worth.

Hold 12+ months after vest for potential LTCG treatment on any additional gain.

None of the fixes are automatic. You have to plan for them before the vest happens.

The people who build real wealth from RSUs treat each vest as a financial event that requires a decision - not a bonus to celebrate and figure out later.

See you next week.

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 2,500+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.