"I Make Too Much for a Roth" Is Only Half True

I hear a version of this almost every week.

Someone makes good money - $200,000, $280,000, sometimes more - and when the subject of Roth IRAs comes up, they wave it off. “I make too much. I can’t do a Roth.” They’ve done enough research to know the income limits exist and stopped there.

That’s half the picture. The other half has been sitting in the tax code since 2010, and the IRS has never closed it.

It’s called the backdoor Roth. Most high earners haven’t heard of it. Some have heard of it but never executed it. And a surprising number are executing it - but doing it wrong in ways that create real, unnecessary tax bills they never saw coming.

Today we’re going through all of it. Let’s dig in.

Why You Can’t Contribute Directly

The IRS restricts direct Roth IRA contributions by income. For 2026: single filers phase out at $153,000-$168,000, married filing jointly at $242,000-$252,000. Above those thresholds, direct contribution is zero.

But here’s what the IRS didn’t close off: there is no income limit on making a non-deductible contribution to a traditional IRA. And no income limit on converting that IRA to a Roth. The backdoor Roth is simply those two steps used together.

How It Works

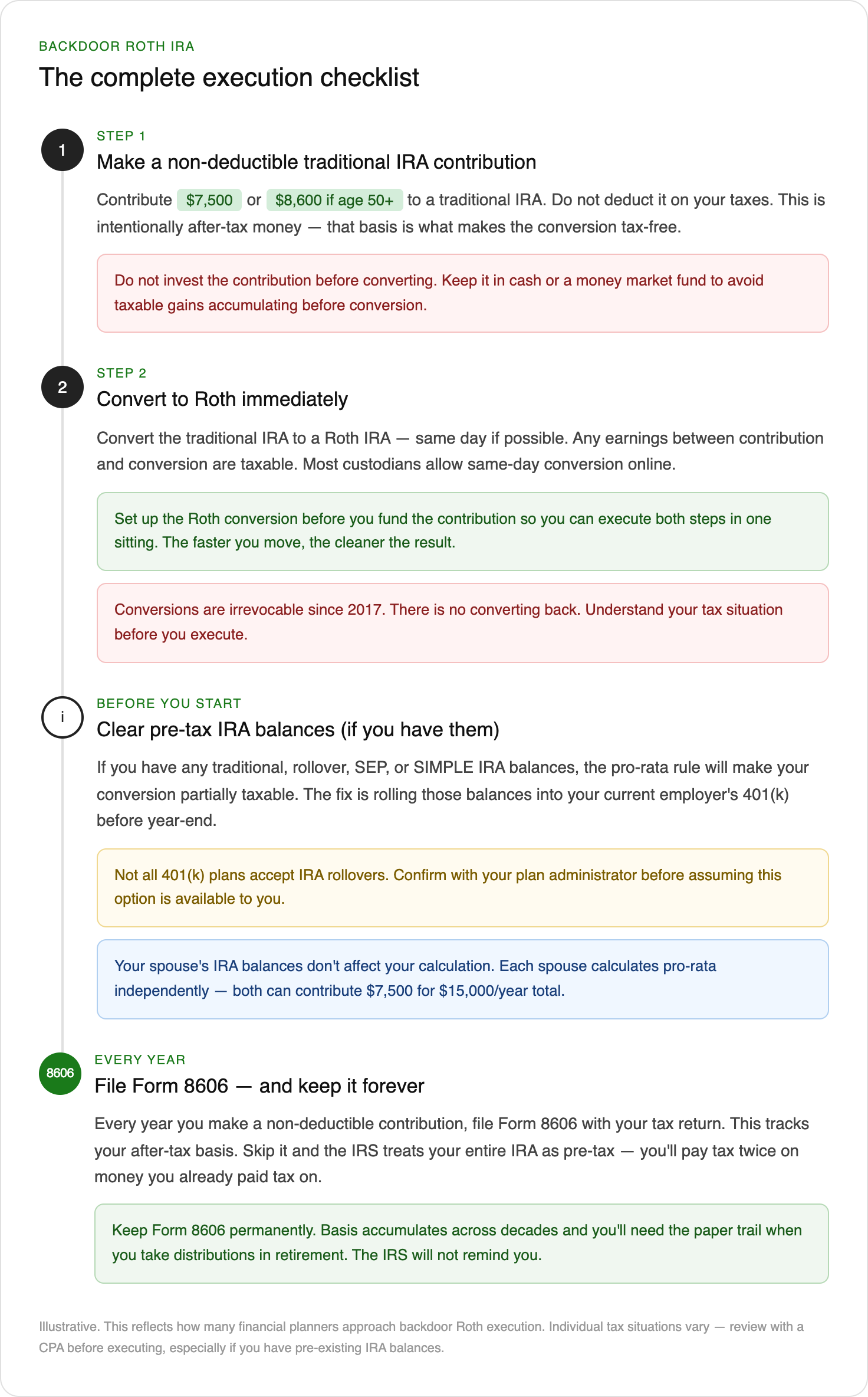

Contribute $7,500 to a traditional IRA - $8,600 if you’re 50 or older in 2026. Critical detail: do not deduct it. You’re putting in after-tax dollars intentionally. That after-tax basis is what makes the conversion tax-free.

Then convert to Roth immediately - same day if possible. Any earnings between contribution and conversion are taxable. A $7,500 contribution that earns $50 before you convert creates $50 of taxable income. Small, but avoidable. Most custodians allow same-day conversion. Set it up before you fund.

Two steps, clean result, $7,500 per year into Roth regardless of income.

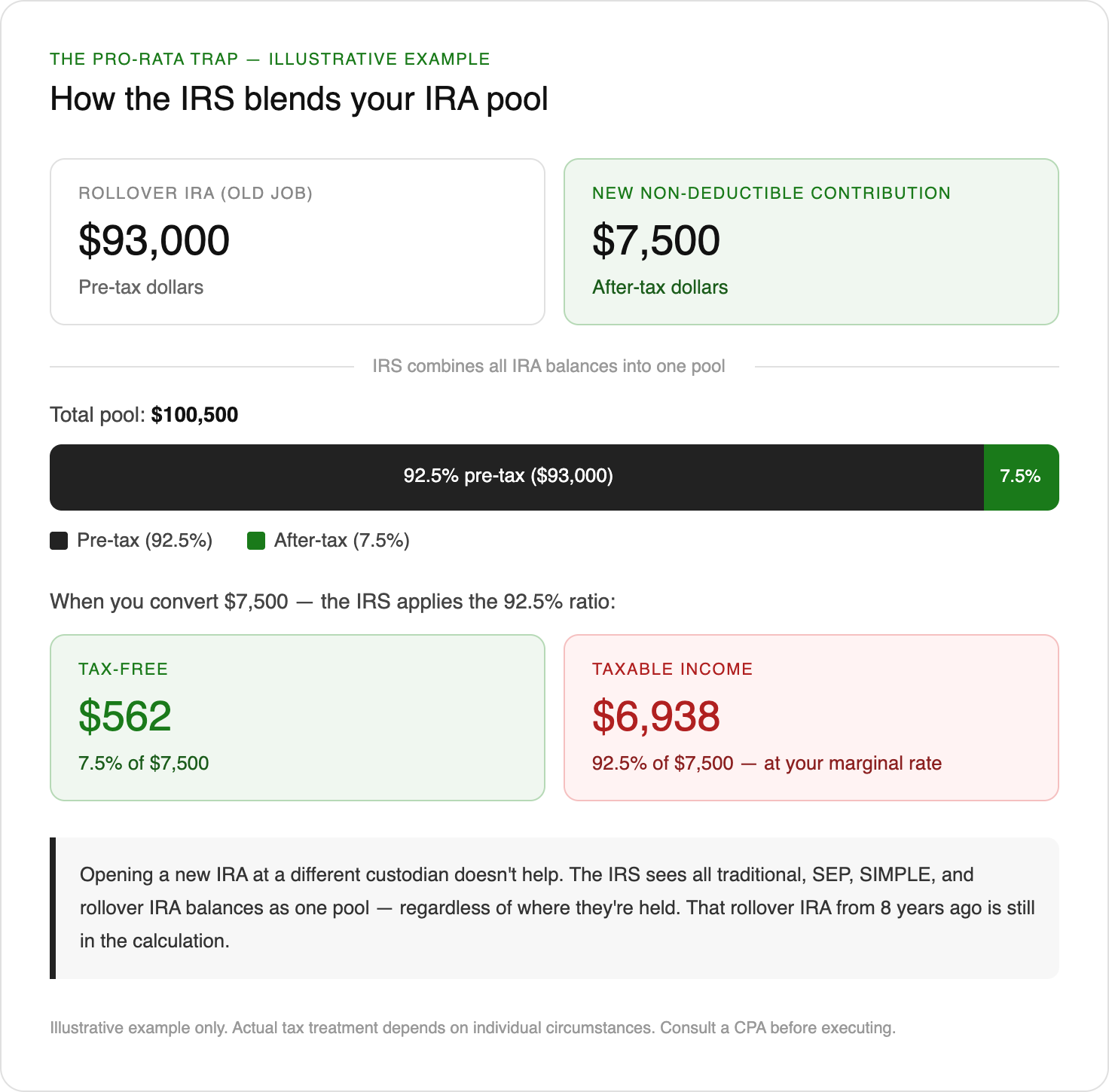

The Pro-Rata Rule: Where Most People Get Hurt

The IRS doesn’t let you choose which dollars you’re converting. It looks at the total of all your traditional IRA balances across every account and every custodian, treats them as a single pool, and applies a ratio. The pre-tax percentage of that pool is the taxable percentage of your conversion.

The graphic below shows exactly what it looks like in a real example:

Opening a new account at a different custodian doesn’t help. The IRS sees through it.

What gets aggregated: traditional, SEP, SIMPLE, and rollover IRAs - everything, regardless of custodian. What doesn’t: 401(k)s, 403(b)s, Roth IRAs. And your spouse’s IRA balances have zero effect on your calculation - pro-rata is calculated independently per spouse, which means both spouses can contribute $7,500 each for $15,000 per year into Roth regardless of household income.

The Fix

The goal most financial planners work toward: $0 in pre-tax IRA balances at December 31 of the conversion year. The most common approach is rolling pre-tax IRA balances into your current employer’s 401(k) before year-end. Since 401(k)s are excluded from pro-rata, this clears the pool entirely.

Important caveat: not all 401(k) plans accept incoming IRA rollovers. Confirm with your plan administrator before assuming this is available to you.

One more thing before you execute: since the Tax Cuts and Jobs Act of 2017, Roth conversions are irrevocable. Recharacterization - converting back to a traditional IRA - is no longer permitted. Understand the tax consequence before you pull the trigger. A partially taxable conversion you didn’t plan for is real income at your marginal rate, with no unwinding it.

The Paperwork That Protects You

Every year you make a non-deductible IRA contribution, file Form 8606. This form tracks your after-tax basis - the record that proves your money was already taxed.

Skip it and the IRS defaults to treating your entire IRA as pre-tax. When you convert or withdraw, you pay tax a second time on money you already paid tax on. The IRS won’t remind you.

File Form 8606 every year. Keep it permanently. Basis accumulates across decades and you’ll need that paper trail in retirement.

The Three Failure Modes

The backdoor Roth isn’t complicated. But it has three specific ways it goes wrong - and none of them are obvious without someone walking you through it.

Pre-existing IRA balances triggering pro-rata on a conversion you assumed would be clean. Waiting to convert so earnings accumulate between contribution and conversion. Skipping Form 8606 so your after-tax basis disappears from the IRS’s records.

All three are avoidable. The steps above reflect how many financial planners approach the execution, but the right setup depends on your specific accounts, your 401(k) plan’s rules, and your tax picture for the year. Worth a conversation with your CPA before you move

.Bottom Line: The Backdoor Roth Playbook

Who it’s for: single filers above $168,000, married filers above $252,000

Pro-rata trap: existing rollover or SEP IRA balances make your conversion partially taxable

The fix: roll pre-tax IRA balances into your 401(k) before year-end - verify your plan accepts rollovers first

Conversions are irrevocable since 2017 - know the tax consequence before you execute

See you next week.

— Fran

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 3,200+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.