The Inherited IRA Lever Most High Earners Never Pull

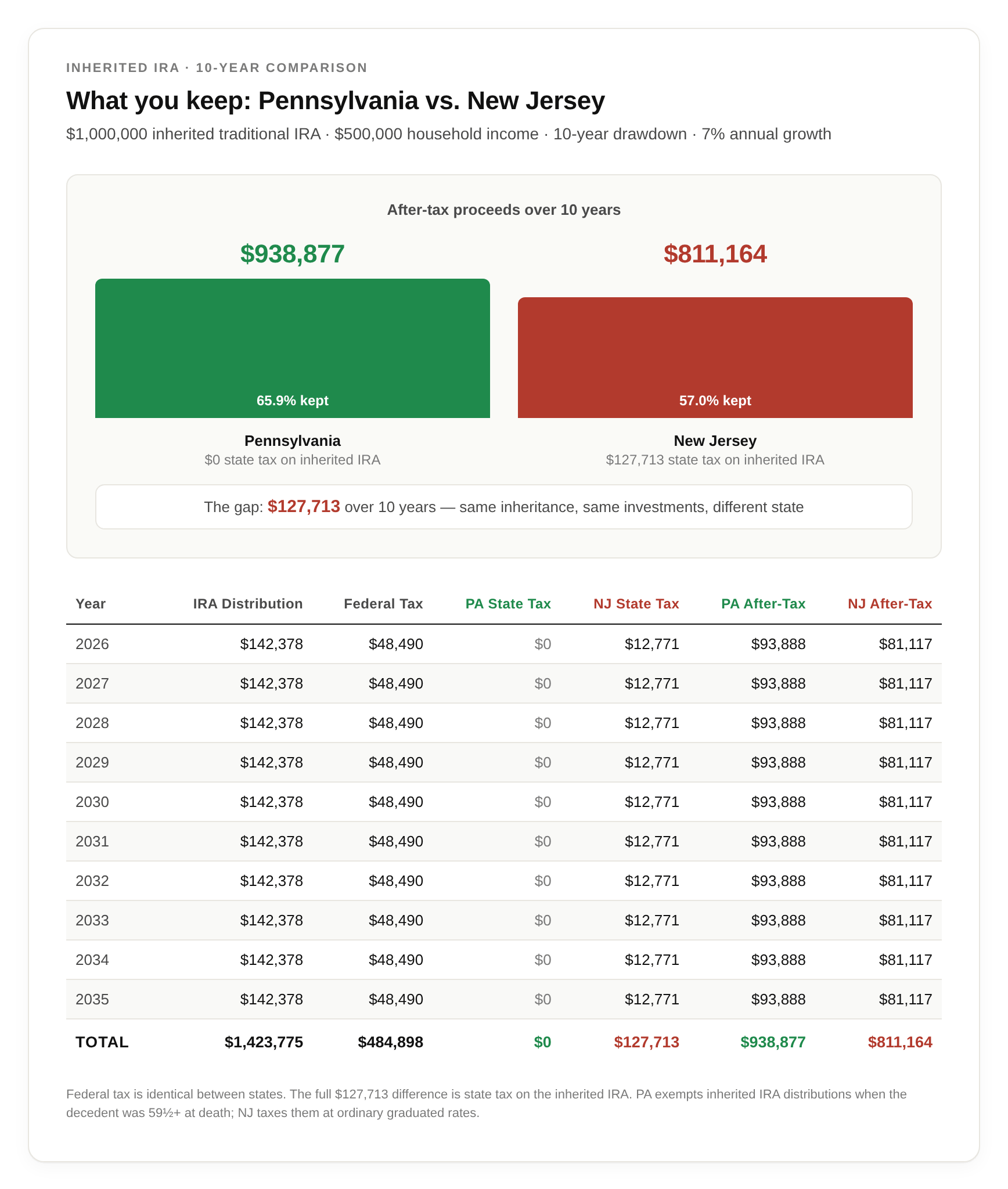

On a $1,000,000 inherited IRA, it's worth $127,713 over ten years.

Two couples inherit a $1,000,000 traditional IRA. Same age. Same household income. Same drawdown plan—ten years, even distributions.

One lives in Pennsylvania.

The other lives in New Jersey, ten miles east.

Ten years later, the Pennsylvania couple has $127,713 more than their neighbors—on the exact same inheritance, with the exact same investments. No tax shelter. No fancy strategy. Just the state where the distributions hit their tax return.

A client of ours is about to inherit a portfolio like this. A family member’s health is failing, and they’re stepping in to help plan around what’s coming.

Residency turned out to be the biggest lever on the table. Most people never realize it’s there.

The bill you’d never see on a Vanguard statement

Most beneficiaries assume the math is simple. You inherit an IRA, the federal government takes its cut, and whatever’s left is yours.

The federal piece is roughly true. Distributions from an inherited traditional IRA stack on top of your W-2 income and get taxed at your marginal federal rate. For a couple earning $500,000 in their primary careers, most of a $1,000,000 inheritance lands in the 32% and 35% brackets. About $485,000 over ten years goes to federal tax. That number is the same in Pennsylvania, New Jersey, California, or Wyoming. Federal tax doesn’t care where you live.

What changes is the second layer.

Pennsylvania exempts inherited IRA distributions from state income tax when the original account owner was over 59½ at death. Every dollar that comes out of that account, principal and growth alike, skips Pennsylvania’s 3.07% flat tax entirely. The state treats it as if the income never happened.

New Jersey doesn’t. Every dollar of a traditional inherited IRA distribution is taxable income in New Jersey, taxed at the same graduated rates as wages. On a $500,000 household income with $142,378 per year in IRA distributions, that distribution lands squarely in New Jersey’s 8.97% bracket.

Over ten years, that’s $127,713 the Pennsylvania couple keeps and the New Jersey couple doesn’t.

Same inheritance. Same investments. Same distribution strategy. A six-figure difference written entirely by which side of the Delaware River you happen to live on.

Pennsylvania and New Jersey happen to make for a clean comparison because they sit ten miles apart with dramatically different rules.

But the same pattern exists wherever you draw the lines. Some states—Florida, Texas, Nevada, Wyoming, and others with no income tax—charge zero on inherited IRA distributions the same way Pennsylvania does. Others tax them in full, with California reaching 13.3% at the top and New York reaching nearly 11% at the highest brackets.

The dollars change, but the mechanism doesn’t.

Why the gap is bigger than it looks

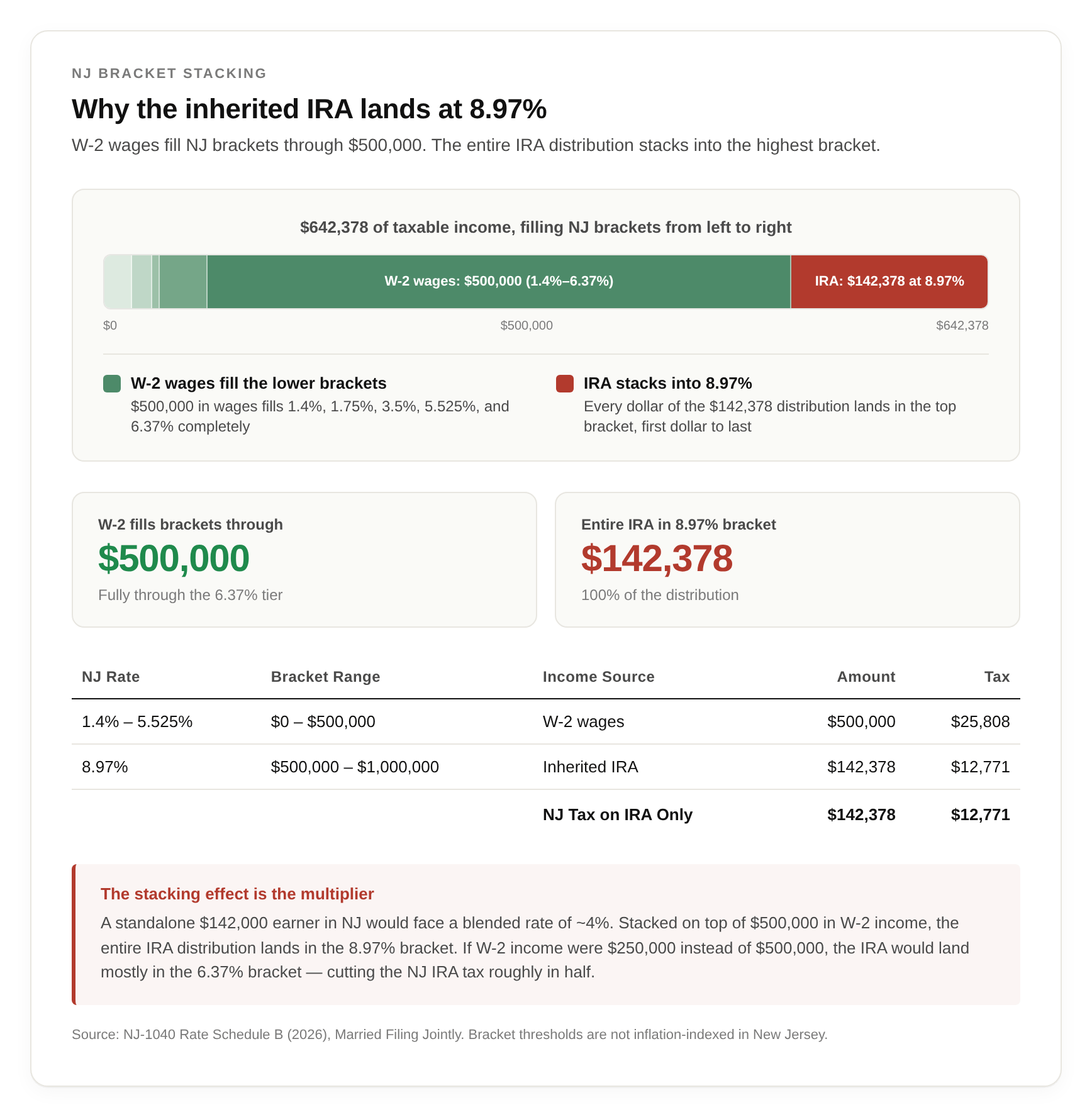

Here’s the part most people miss. When you read “New Jersey taxes IRA distributions up to 10.75%,” it’s easy to assume the average rate would be modest. Spread across the lower brackets, you’d expect something closer to 4 or 5%. That’s not how it works for high earners.

By the time your W-2 income hits $500,000, you’ve already filled New Jersey’s lower brackets. The 1.4% bracket, the 1.75%, the 3.5%, the 5.525%, the 6.37%, all spoken for by your wages. So when the inherited IRA distribution arrives on top of that, it doesn’t start at the bottom of the tax table. It starts where your wages left off, which is the 8.97% bracket.

The whole distribution lands there. Every $142,378 of inherited IRA income, every year, taxed at 8.97% from the first dollar to the last.

A standalone $142,000 earner in New Jersey would face a blended effective rate around 4%. A $500,000 earner inheriting that same IRA pays more than double on the exact same dollars. The distribution lands on top of an already-stacked tax return, and the entire amount falls into the highest bracket your wages reached.

This is the part most “tax-friendly state” articles miss. The headline rate is one thing. The stacking effect is what actually empties the account.

It also means the lever has the most value for the people earning the most. Cut the household income to $250,000 and the IRA mostly lands in the 6.37% bracket. Still painful, but the gap narrows. At $750,000, it’s worse than the example above. The higher you earn, the more your state of residence is doing to your inheritance.

When residency actually becomes a lever

So the gap is real, and it compounds. Now the harder question: what do you actually do with this?

The answer most articles jump to is *move.* That’s not the answer for most people.

Uprooting your life to save state income tax is rarely the right trade. Family lives where they live. Careers anchor where they anchor. The math has to clear a much higher bar than “I’d save money,” because the cost of the move, social, professional, geographic, is real.

But there’s a smaller version of this decision that gets ignored.

Sometimes a move is already on the table for other reasons:

A job change or relocation

A downsize after the kids leave

A partner’s career move

A shift to remote work that uncouples your job from your zip code

A planned sabbatical or career break

In those moments, the timing of when you cross the state line, relative to when you take inherited IRA distributions, becomes one of the highest-impact decisions in your financial life.

The federal rule that makes this work was passed in 1996. Federal law prohibits a former state from taxing IRA distributions you take after you’ve established residency elsewhere. Once you’ve established residency in a new state, your former state can’t reach into your inherited IRA. The state where you live when the distribution hits is the only state with claim on it.

A few things to know if you’re sitting with this decision:

Domicile is what matters. Domicile is your permanent legal home, where your real life is centered. States look at where your driver’s license is issued, where you vote, where your kids go to school, where your doctors and accountants are, where you spend the bulk of your nights. States like New York and New Jersey audit these decisions aggressively, and they look at the totality of your life pattern, not any single factor.

Timing is binary. Distributions taken before you change residency are taxed by the old state. Distributions taken after are taxed by the new one. There is no proration. Whatever your residency is on the date the distribution hits, that is the state with claim on it.

The 10-year window gives you a runway. If a move is realistic in years three or four of the 10-year window, deferring distributions into the post-move years can capture the lever without forcing the move itself to happen sooner than it should. This is where last week’s distribution-pacing strategy compounds with residency.

The lever has value even if you never pull it. Knowing what residency is worth is part of understanding your full financial picture. Some readers will move and use this. Most won’t. Both should leave with a clearer view of the costs and trade-offs sitting inside the inheritance.

The point isn’t to chase tax savings around the country. The point is that residency is one of the most underused inputs in financial planning. For high-earning beneficiaries of an inherited IRA, it might be the single biggest dollar lever on the table. Most people never realize it’s there until the account is empty.

That’s it.

Our client called because a family member’s health is failing, and a $1,000,000 inherited IRA is about to land in their lives. They expected the conversation to be about how to invest it. It turned into a conversation about where to live.

That’s the part most people don’t see coming. An inherited IRA isn’t just a number on a statement. It’s a ten-year tax decision wearing the disguise of an inheritance. Federal tax is fixed. Investment returns are uncertain. Residency is the one input you actually control, and for the people earning the most, it moves the most money.

Most readers won’t move. Most shouldn’t. But knowing what residency is worth is its own kind of wealth.

Now you know what’s on the table.

Thanks for reading. See you next week.

— Ryan

Whenever you’re ready, there are 2 other ways we can help you:

Join The Opulus Method Newsletter — Every Tuesday, I share strategies that help high-income millennials build wealth without sacrificing their life. Join 3,200+ readers.

Work With Us 1-on-1 — We’ll build your personalized strategy to cut your taxes, maximize your income, and grow your wealth month after month. You focus on living your life. We handle the financial strategy and execution.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.